Startup Spotlight: genOTC is Rewriting the Math of Modern Financial Markets

In modern financial markets, pricing, hedging, and risk decisions all hinge on volatility modelling. Yet volatility is not directly observable. It has to be inferred from the prices of listed vanilla options and represented as a surface that encodes forward-looking market expectations across strikes and maturities.

This is where conventional calibration approaches start to fail.

The Fragile Art of Modeling Volatility

The drift term, which captures an asset’s long-term direction, is rigidly set by no arbitrage conditions. Volatility is not. “Volatility is far more challenging,” explains Dr. Benjamin Joseph, Quantitative Researcher and Lead Core App Developer at genOTC. “Current models rely on simplifying parametric assumptions you wouldn’t necessarily want to impose; they are fragile and unstable. When these assumptions break, your model will struggle to replicate what the market is telling you.”

Most institutions rely on parametric families such as SVI or SABR that impose rigid structural assumptions on the surface or maintain in-house local volatility fits that require continuous recalibration and oversight. Both approaches can break under regime shifts, introduce arbitrage, and leave desks exposed to model risk, hedging error, and costly mispricing.

This persistent and expensive challenge has created room for a new generation of calibration technology. genOTC is reformulating the calibration problem from first principles, using optimal transport theory to produce arbitrage-free local volatility surfaces consistent with observed market data.

genOTC is not building another analytics dashboard or trading platform. It is building an arbitrage-free local volatility modeling and pricing engine, delivered as an AI-native platform built on optimal transport. Expressing calibration as a convex optimal transport problem gives a unique solution that matches market data and produces a smooth local volatility model suitable for pricing path-dependent exotics.

However, behind this apparent simplicity lies a strong mathematical challenge, the one that genOTC is tackling.

Building a Platform to Serve the Industry

Banks pricing path-dependent exotics such as autocallables, hedge funds developing systematic options strategies, and independent price verification teams all face the same requirement. They need models that are consistent with market prices. genOTC’s platform is built to deliver exactly that.

Users can upload their own data or use data sourced by genOTC, and the system generates an arbitrage‑free local volatility model using the company’s model‑free, optimal‑transport‑based approach. As Joseph describes, their methodology “works directly on the market data using the language of optimal transport.” Because the framework imposes no parametric form on the surface, the resulting model is arbitrage-free by construction and applies across asset classes without bespoke reformulation.

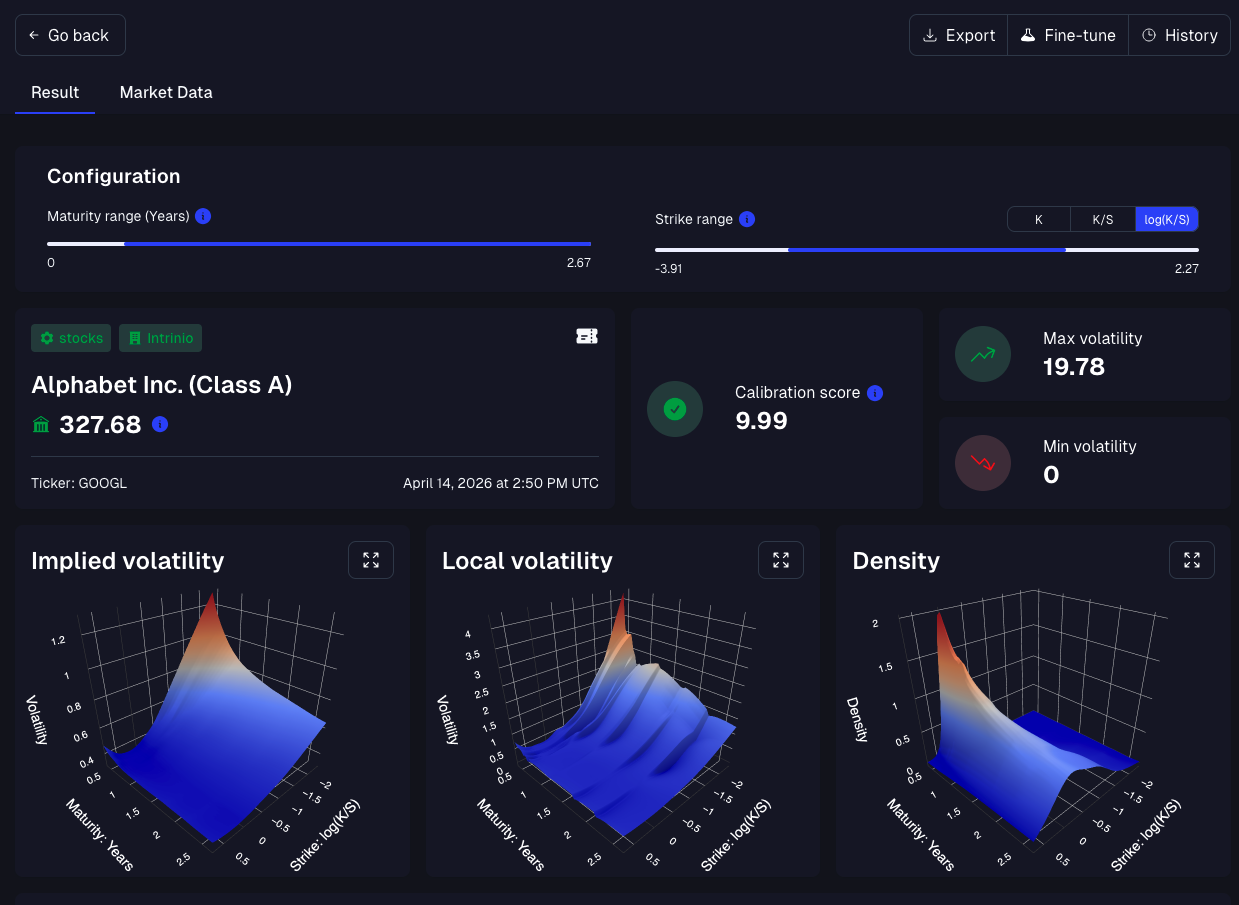

The genOTC app interface showing GOOGL (Image courtesy of genOTC)

Once calibrated, the platform becomes a workspace for analysis. Users can inspect implied and local volatility surfaces, evaluate how well the model matches input data, and understand its behavior through intuitive visualizations. From there, the calibrated model can be exported into pricing libraries for solving PDEs or running Monte Carlo simulations, which are essential tasks for fair pricing of over-the-counter derivatives. “Because you can’t just observe the market price [of an exotic], it’s important that you have a well-calibrated model that can tell you a fair price,” Joseph notes, underscoring the value of a reliable calibration engine.

For teams building automated workflows, the same functionality is available via an API, enabling scripted calibration and seamless integration with existing systems. The result is a workflow engineered for quants but accessible to anyone who relies on accurate models for financial decision‑making.

MATLAB Accelerates FinTech Development

Behind this workflow is a computationally intensive numerical engine. To build it, genOTC relies heavily on MathWorks tools. Joseph says, “We use optimal transport and PDE-driven techniques to create a local volatility model consistent with some given market data. Therefore, one of the key ingredients of our methodology is solving many PDEs numerically.” To achieve these results, the team relies critically on efficient linear algebra solvers, heavily uses vectorization capability, two things that MATLAB does very well.

“The ease of development with MATLAB cannot be overstated. The ability to quickly create toy experiments and visualize the results using MATLAB’s market-leading plotting software has greatly sped up the development of our algorithm.” – Benjamin Joseph, Quantitative Researcher and Lead Core App Developer, genOTC

The team uses MATLAB throughout their development workflow. MATLAB is used to write and test functions, plot three-dimensional volatility surfaces, run experiments, and iterate at a pace suited for research-heavy development. The Financial Toolbox and Optimization Toolbox are used as foundations for common financial calculations, including validation and regression tasks. When they’re ready to deploy, they compile the MATLAB code using MATLAB Compiler, package it into a Docker container with MATLAB Runtime, and run it on AWS EC2.

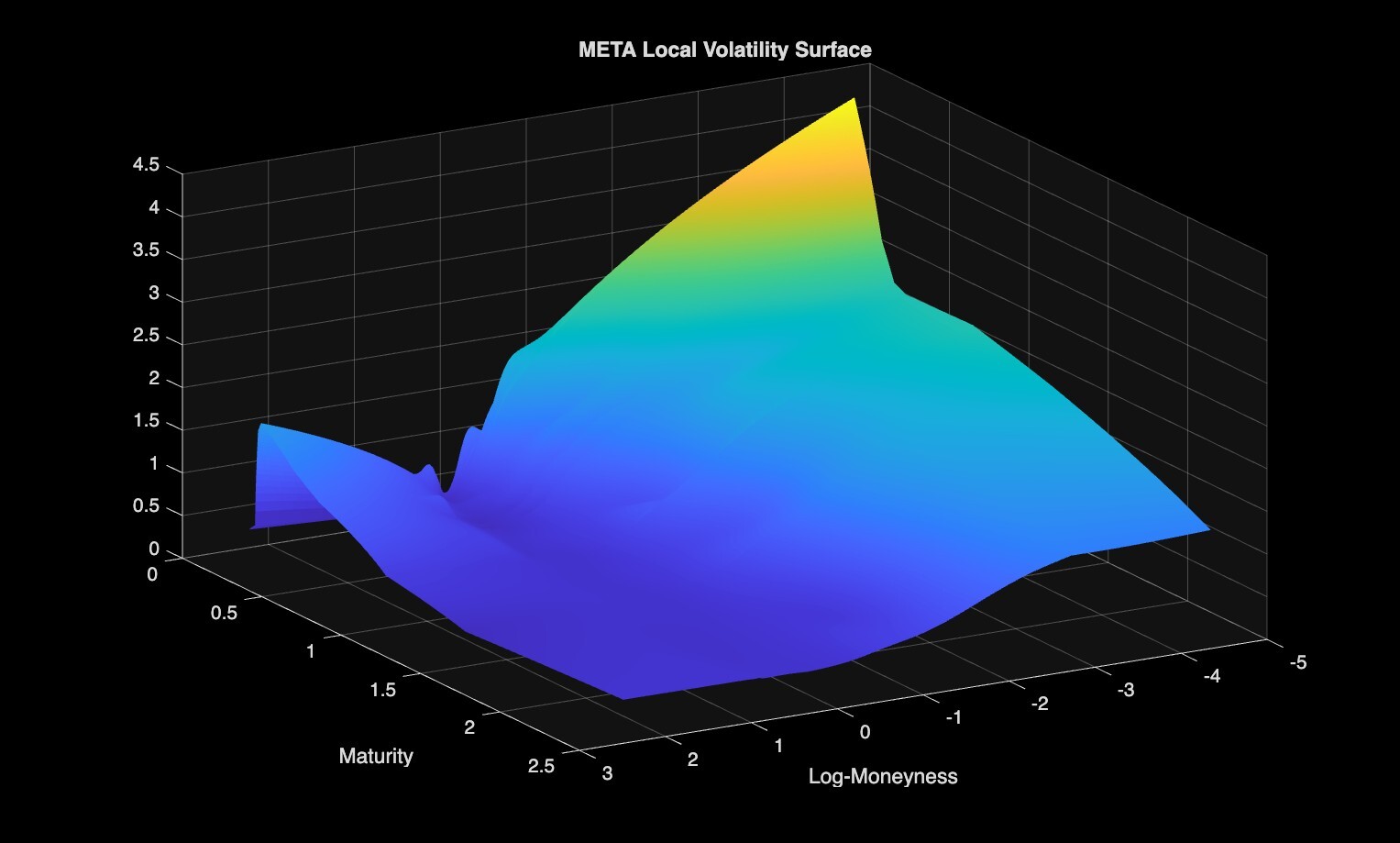

Visualization of META Local Volatility Surface – an example of MATLAB’s 3D plotting capabilities (Image courtesy of genOTC)

The team has drawn on multiple MathWorks resources throughout development. Engineering support and the MATLAB Answers forum have resolved implementation questions quickly, while the MATLAB Profiler has helped identify bottlenecks and improve the algorithm’s performance on computationally complex operations. “The addition of MATLAB Copilot has enhanced our workflow, with most routine questions rapidly answered,” says Joseph.

As genOTC’s team continues to grow, they anticipate expanding their use of MathWorks software, adding licenses to support both the quant and software development teams. Unlike traditional providers in the space, limited to providing services during business hours, genOTC’s AI-native platform will give market participants 24/7/365 access to a full workbench of services as a one-stop-shop for options, including: calibration-as-a-service, pricing, backtesting, and quant libraries. “With robust software, responsive support, and tools like MATLAB Copilot, MathWorks has been and will continue to be instrumental in helping our team streamline workflows and deliver more robust and reliable insights to market participants,” concludes Joseph.

Expanding Across Asset Classes and Users

genOTC has already calibrated models to equity index markets with European-style options, single-name equities with American-style options, and cryptocurrency markets. FX is currently in benchmark testing, with commodities and fixed income next in line. Despite the diversity of these markets, the underlying algorithm remains unchanged. What shifts is the data environment around it, not the modeling framework.

genOTC recently reached a milestone with the fall 2025 launch of an early version of their calibration tool. They are now expanding their AI-native workbench to include a pricer, backtesting capabilities, and a quant library, which are already available to select clients through co-development. The team is also broadening asset class coverage and partnerships while preparing for a Series A fundraise.

A Team Driven by Mathematics and Momentum

For Joseph, the work is deeply personal. His PhD work was about the theoretical foundations of calibration by Optimal Transport. genOTC allows him to explore the next question: how do we make it work every day, for real customers, in real markets?

The startup’s team of quantitative researchers is tackling open questions at the intersection of optimal transport and mathematical finance while delivering production software. The bar is high, and the pace reflects a group focused on translating rigorous research into tools desks can actually rely on.

genOTC is bringing a mathematically grounded, disruptive approach to one of the most persistent problems in quantitative finance. Paired with the right engineering tools, rigorous research reaches production, and market participants get pricing models they can rely on.

- Category:

- Startup Spotlights

Comments

To leave a comment, please click here to sign in to your MathWorks Account or create a new one.