Under SR 26-2, Misclassification Is the New Model Risk

When materiality determines rigor, classification becomes a first-order governance issue.

Series introduction

The first two blogs in this… read more >>

Under SR 26-2, Misclassification Is the New Model Risk

When materiality determines rigor, classification becomes a first-order governance issue.

Series introduction

The first two blogs in this… read more >>

Where SR 26-2 Creates Flexibility—and Where It Does Not

The opportunity is real, but it is narrower, more conditional, and more defensible-on-paper than a first read suggests.

Series… read more >>

SR 26-2 Did Not Lighten the Load. It Moved the Burden of Proof.

The real change is not the shorter guidance. It is the centrality of defensible judgment.

Series introduction

This is the first in a… read more >>

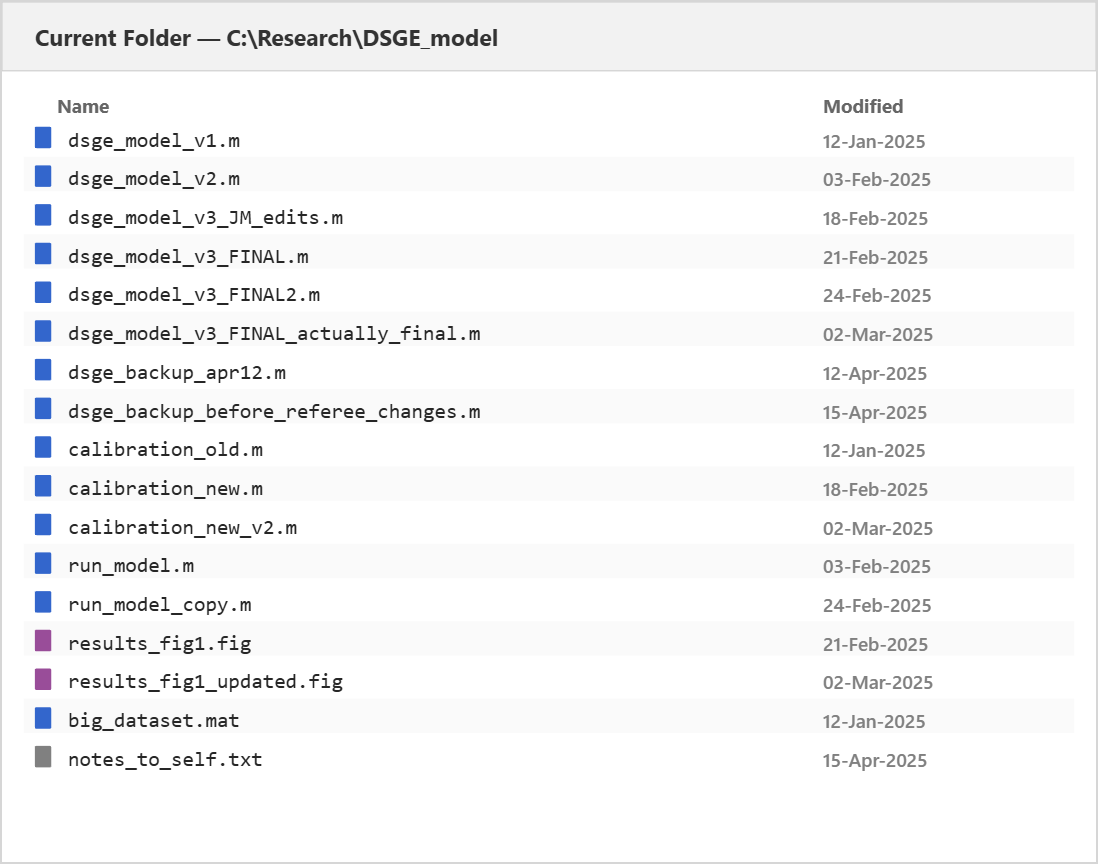

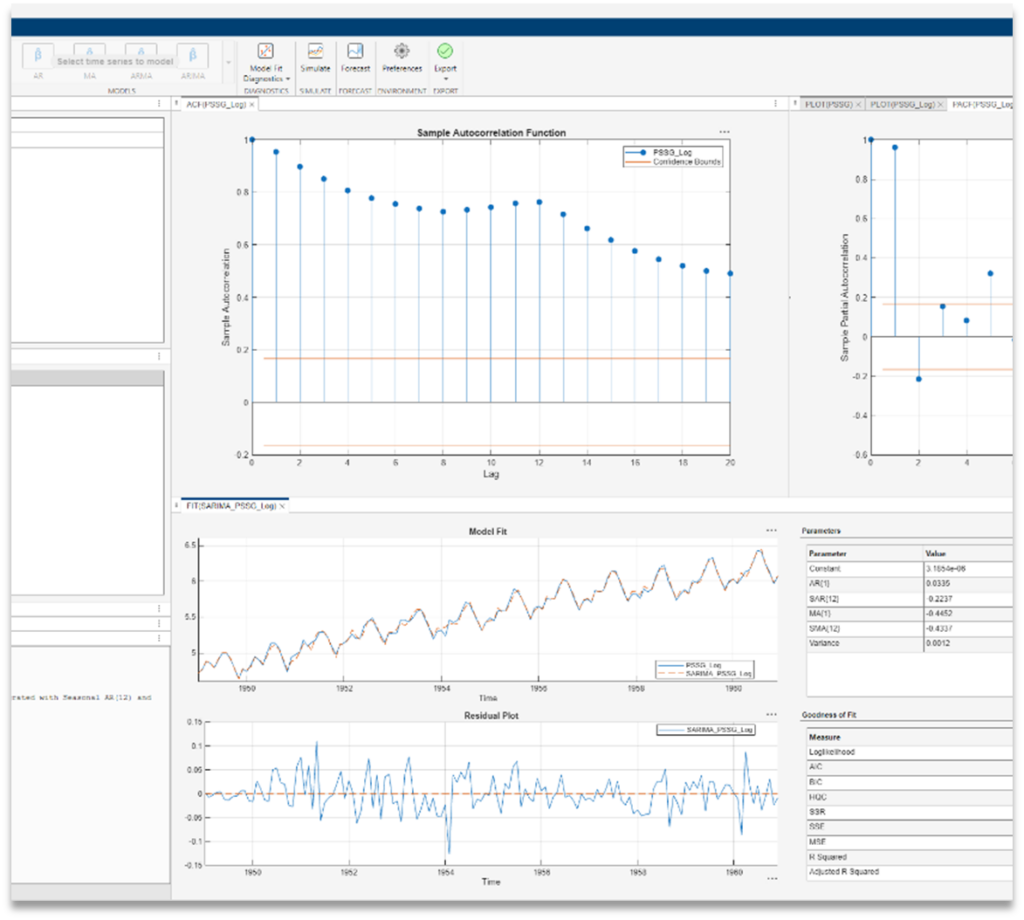

A Practical Guide to Git in MATLAB

The Problem You Already Have

You know the folder. Somewhere on your machine there is a directory that looks like this:

A familiar sight: version history encoded… read more >>

Economists often keep years of work in EViews workfiles: macroeconomic series, model estimates, and curated panel data. The MATLAB Reader for EViews Workfile reads .wf1 and .wf2 files into MATLAB,… read more >>

A practical MATLAB walkthrough comparing tracking error and exact exposure approaches.

When you build a factor-based portfolio, the central design choice is how strictly to enforce your factor… read more >>

Expert Contributor: Dr. Yuchen Dong

Yuchen is a Senior Application Engineer at MathWorks focusing on customers in the financial services industry. His focus areas are financial instruments,… read more >>

Expert Contributor: Dr. Eduard Benet Cerdà

Edu is a Senior Application Engineer at MathWorks advising customers in the development and deployment of financial applications. His focus… read more >>

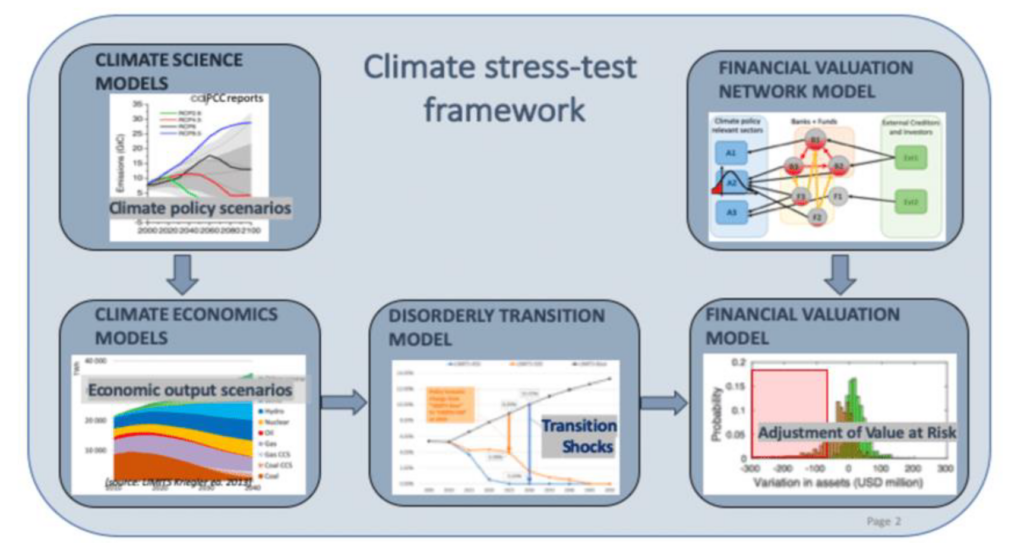

R2026a covers a lot of ground for economists—Bayesian state-space estimation, macro-scale forecasting, climate and physical risk mapping, symbolic dynamics, and AI-assisted model review, among… read more >>

Effective risk management increasingly requires understanding how climate‑related factors can influence market valuations and balance‑sheet resilience. CRISK provides a transparent, market‑based… read more >>

These postings are the author's and don't necessarily represent the opinions of MathWorks.