Climate Risk in Finance: Insights from Our Comprehensive Executive Panel Discussion

The following blog was written by Arpit Narain from the MathWorks Finance team.

1. Introduction

In today’s financial landscape, climate risk has taken center stage, demanding the attention of industry leaders. MathWorks recently hosted an executive panel discussion in NYC that convened top-tier executives from financial institutions, each responsible for managing climate risk within their organizations.

Our panel featured esteemed thought leaders and industry experts, including David Carlin (Head of Climate Risk & TCFD at the United Nations Environment’s Program for Financial Institutions – UNEPFI), C. Robin Castelli (Head of Climate Modeling Analytics at Citi), and Rishi Desai (Head of Sustainability Risk Architecture at UBS). It was moderated by Arpit Narain (Global Head of Financial Solutions at MathWorks). Together, they delved into pressing topics reshaping climate risk management in finance.

Throughout the discussion, the panel explored the evolution from Task Force on Climate-related Financial Disclosures (TCFD) to International Sustainability Standards Board (ISSB), expectations from the Securities and Exchange Commission (SEC) disclosure rules, complexities of regulatory climate scenario exercises, and practical applications of scenarios in climate stress testing. They also shared insights on best practices for sourcing data, building and validating climate risk models, and persistent implementation challenges within the financial sector.

This blog captures the essence of insights shared during this panel discussion, offering a concise perspective on navigating the evolving landscape of finance and climate risk management.

2. Understanding the TCFD to ISSB Transition in Financial Institutions

a. TCFD’s Journey and ISSB’s Emergence

By the end of 2021, TCFD achieved mainstream adoption in North American and European markets. However, its reach was limited in regions where majority of global emissions and climate risks are concentrated. The transition from TCFD to ISSB marks an evolution in climate risk disclosure, retaining core TCFD principles while expanding detail and scope. This shift will potentially address the uneven global adoption of TCFD guidelines, especially in regions with significant climate risks.

b. ISSB’s Enhanced Framework

The ISSB builds upon and elaborates the TCFD structure. This transition is seen more as an “evolution than a revolution”, with ISSB enhancing and expanding on TCFD’s foundational work. Despite different accounting standards like the Generally Accepted Accounting Principles (GAAP) in the U.S., the ISSB’s standards (S1 and S2 for sustainability and climate) are designed to be agnostic to specific accounting frameworks. A well-structured ISSB report will inherently align with TCFD standards, reducing the need for separate reporting efforts.

c. Regulatory Adoption and Interoperability

The ISSB actively integrates work from various bodies like the CDSB (Climate Disclosure Standards Board), SASB (Sustainability Accounting Standards Board), GRI (Global Reporting Initiative), and EFRAG (European Financial Reporting Advisory Group), fostering a more interoperable and unified approach to climate reporting. The transition is expected to encourage more rapid adoption of climate disclosure standards by regulators, particularly those who haven’t yet mandated such structures.

3. Expectations from the Upcoming SEC Disclosure Rules

a. Key Principles and Goals

Inspired by the TCFD, the SEC climate disclosure rules aim to reduce information asymmetries and failures, enhancing market functionality and stability. These rules focus on standardizing and validating financial disclosures, ensuring that they provide a comprehensive and transparent view of a company’s financial health.

b. Implications for Disclosure Practices

The rules are designed to ensure comprehensive disclosure by firms, preventing selective reporting and enhancing transparency. The primary objective is to make disclosures more useful for investors, aiding in informed decision-making.

c. Challenges and Speculations

The postponement in releasing the SEC rules is causing apprehension in the industry, potentially placing U.S. entities at a comparative disadvantage globally. This lag creates uncertainties regarding compliance and efficient use of resources in anticipation of new regulations. Also, there is speculation that the upcoming rules might be moderated, particularly in areas like scope three emissions and scenario analysis. This could lead to phased rollouts, safe harbor provisions, or optional compliance elements, potentially diluting the initial robustness of the proposed regulations.

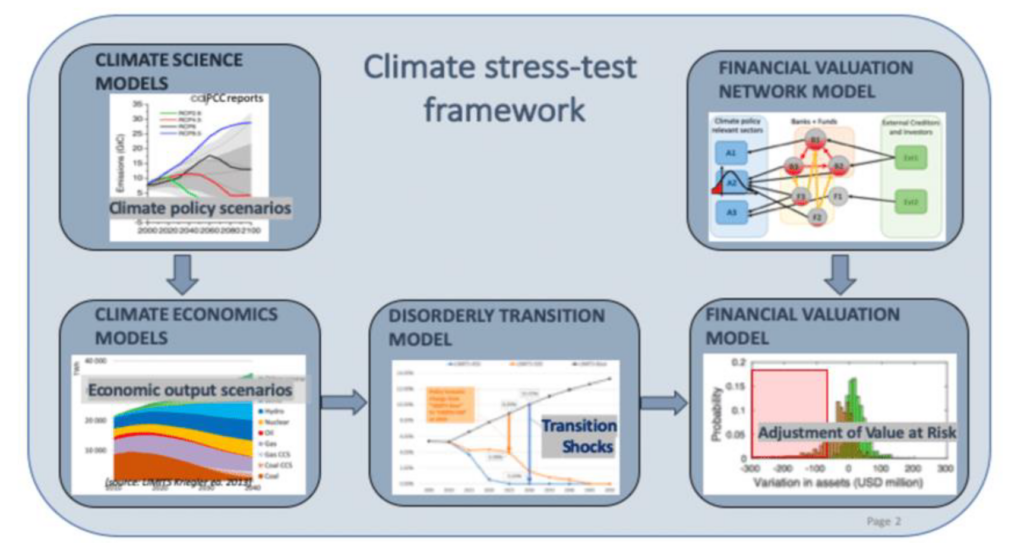

4. Key Aspects of Leading Regulatory Climate Scenario Exercises and Comparisons

a. Exploratory Nature and Capital Implications

The Federal Reserve Bank’s Climate Scenario Analysis (CSA) was highlighted as an exploratory exercise, distinct from stress tests due to its lack of capital implications. Such exercises are increasingly aligning with European approaches, covering pretty much the entire book. It’s noteworthy that the short-term, 10-year focus of the US exercise contrasts with the typically longer 30-year transition scenarios which is needed to better understand the risks banks face to their safety and soundness.

b. Dynamic Balance Sheet Modeling

To conduct a “true” stress testing exercise, it’s essential to transition from static to dynamic balance sheet modeling. However, moving from the traditional Comprehensive Capital Analysis and Review (CCAR) frameworks, which typically project up to nine quarters ahead, to modeling 30-year climate risk scenarios, significantly increases uncertainty. This shift presents a substantial challenge in accurately forecasting long-term financial impacts, becoming a crucial focus area for both financial institutions and regulators.

c. Integration into Regular Stress Tests

Regulators are pushing for the integration of climate considerations into standard stress tests, such as the Current Expected Credit Loss (CECL), CCAR, and IFRS 9. This approach aims to make climate risk a fundamental part of routine risk management processes.

d. Systemic Approach and Network Effects

Some advanced state exercises, like those conducted by Swiss banks with Financial Market Supervisory Authority of Switzerland (FINMA), focus on network effects at a micro level. These exercises delve into the systemic nature of risks, emphasizing the need for more complex and nuanced models to capture the uncertainties of climate risks at the counterparty level.

e. Need for Enhanced Modeling Techniques

The speed of regulatory response sometimes outpaces the development of sophisticated models. There is a need for more advanced understanding of transition risks, encompassing factors like operational and indirect costs, technological impacts, and market shifts.

f. Decision Usefulness

The primary objective of these exercises is to enhance the understanding of supervisors and institutions about climate risks. This involves defining terms and approaches, systematically discussing risks across the industry, and focusing on short-term shocks and second-order effects. The goal is to make these exercises more decision-useful for policymakers and financial institutions.

g. Future Developments

There is a growing awareness of the value of these exercises in preparing for the future. However, to make them truly informative and usable for stability and decision-making, there needs to be a focus on new parameters, including short-term scenarios and understanding correlations between various hazards.

5. Applying Scenario Analysis in Business Context Beyond Regulatory Exercises

a. Integration with Existing Risk Management Practices

Banks are focusing on making scenario analysis decision-useful by downscaling factors such as market risk shocks to more practical timeframes, like three days. This involves integrating climate risks with other existing issues, such as geopolitical tensions, moving beyond the siloed approach traditionally used in risk assessment. This integration is seen as a critical step towards a comprehensive understanding of risks in a real-world business context.

b. Modular Approach in Model Development

The development of climate models is being approached modularly, allowing for flexibility and adaptability. This involves thinking in terms of a ‘climate premium’, which isolates the impacts of transition and physical risks from broader macroeconomic variables. Layers and submodels addressing legal liabilities, physical impacts on assets, contagion, and network effects are added modularly. This approach leverages existing frameworks used in stress tests like CCAR and IFRS 9, ensuring that new models are integrated into validated, operational systems.

c. Linking Models to Business Practices

The objective of scenario analysis exercises should be to ensure that they serve not merely for regulatory compliance but are actively utilized to bolster business resilience and sustainability. This can be accomplished by establishing a connection between theoretical models and real-world business practices, ensuring that preparations for potential climate risks are substantive, effective, and actionable.

6. Best Practices for Sourcing Data, Integrating, and Validating Climate Risk Models

a. Centralized data management

A pivotal practice at some of the financial institutions involves the centralization and standardization of data sourcing across the institution. By standardizing vendors and developing a framework to ensure data quality, the financial institutions can streamline data distribution through the cloud. Centralized sourcing also enables more effective negotiation with vendors to fill data gaps and improve data quality.

b. Addressing outdated vendor data

Financial institutions face challenges with vendor data that may be out-of-date, an example of which could be a failure to capture recent significant Capital Expenditure in a client’s transition plan. To counter this, some institutions implement parallel data tracks within their internal systems, equipped with audit trails to ensure proper governance and validation. They place a strong emphasis on the governance of these new data inputs, focusing on maintaining accuracy, timeliness, and seamless integration into their climate risk models.

c. Modeling and Validation of Transition Risk in Credit Assessments

Integrating transition risk into internal credit rating models, crucial for loss forecasting, faces significant hurdles. The primary challenge is the scarcity of relevant historical data, which restricts the scope for independent backtesting of these models. Consequently, these models must initially rely on expert-driven approaches until sufficient data accumulates to enable comprehensive testing against other datasets. Banks are adopting a dual strategy to address these challenges, which includes (1) amalgamating scores from various agencies, banks create their own composite ratings, enhancing the robustness of their assessments, and (2) promoting collaboration between model validation and development teams to improve internal credit rating models, allowing for continuous refinement, especially as more data becomes available.

7. Key Climate Risk Implementation Challenges and Best Practices in Financial Institutions

| # | Challenge | Best Practice |

| 1 | Resourcing & Skills

Innovation in climate risk space, whether it’s about validation, the review process, or building, often outpaces the resources and speed of implementation in institutions. |

Conducting Specialized Trainings

Develop specialized training to ensure that staff is up-to-date with the latest developments and tools. |

| 2 | Data Collection and Analysis

New challenges arise in collecting and analyzing data types that were previously not considered, such as scope three emissions and physical hazards. |

Developing Robust Data Frameworks

Developing robust frameworks for data collection and analysis is key. This includes standardizing data sourcing, ensuring data quality, and continuously adapting to fill in data gaps. |

| 3 | Model Development and Validation

Building and validating new models for climate risk is challenging, as these models are relatively new, and some fundamental relationships may not hold. |

Collaborative Model Development

Leveraging collaboration platforms to work closely with model validation teams and using a collaborative approach in model development is essential. This collaboration allows for the creation of more robust and accurate models. |

| 4 | Integration and Usage

The climate risk models and processes are often not well integrated with the existing business-decisioning and risk management framework. |

Integrating Climate Risk into Business Processes

Integrating climate risk considerations into every aspect of the business, from risk management to client engagement and decision-making, is crucial. This involves defining a clear risk appetite, developing end-to-end processes for climate risk management, and ensuring these processes become a part of the institution’s DNA. |

| 5 | Ownership and Authority in Risk Management

Determining ownership and authority for climate-driven credit risks within the organizational structure can be complex, especially when integrating sustainability risks into traditional risk management frameworks. |

Clear Definition of Roles and Responsibilities

Defining clear roles and responsibilities for managing climate risks and establishing processes for transferring underwriting authority and decision-making between teams are important. This also involves integrating climate risk experts into core business units to ensure effective risk management. |

8. Key Takeaways

- The shift from TCFD to ISSB signifies an evolution in climate risk disclosure, fostering a unified global approach.

- Anticipation surrounds the SEC Disclosure Rules, but delays and potential moderation introduce uncertainties.

- Regulatory climate scenario exercises evolve to align with European approaches, emphasizing enhanced modeling techniques.

- Financial institutions should consider centralizing data management and extending scenario analysis beyond compliance by integrating climate risks into their existing business risk management processes.

- Specialized training, robust data frameworks, and collaborative model development are vital for overcoming climate risk challenges in financial institutions, enhancing resilience and sustainability.

9. Call to action

As we continue to navigate the complexities of climate risk, MathWorks is committed to playing a pivotal role in developing innovative solutions and strategies. Our dedicated team is focused on leveraging advanced analytics and modeling tools to better understand and mitigate climate-related risks. The details of MathWorks’ Climate Risk offerings can be found here.

For more information about our initiatives or to discuss potential collaborations, please feel to contact Arpit Narain (anarain@mathworks.com) or Akshay Paul (apaul@mathworks.com)

- Category:

- Climate Finance

Comments

To leave a comment, please click here to sign in to your MathWorks Account or create a new one.