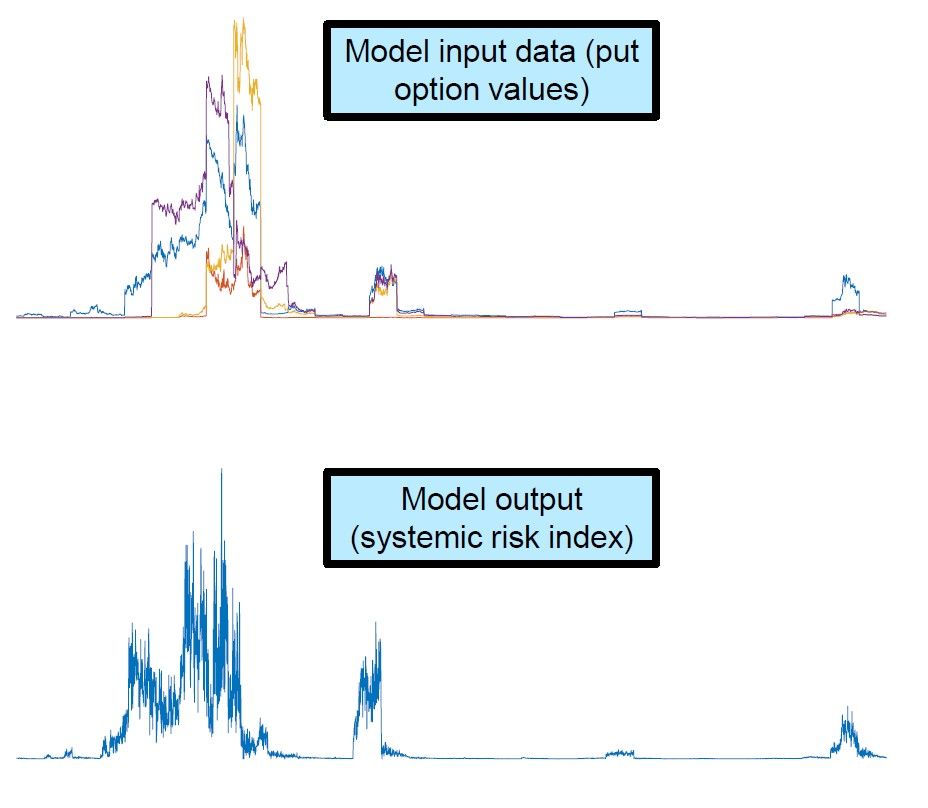

Effective risk management increasingly requires understanding how climate‑related factors can influence market valuations and balance‑sheet resilience. CRISK provides a transparent, market‑based… read more >>

Effective risk management increasingly requires understanding how climate‑related factors can influence market valuations and balance‑sheet resilience. CRISK provides a transparent, market‑based… read more >>

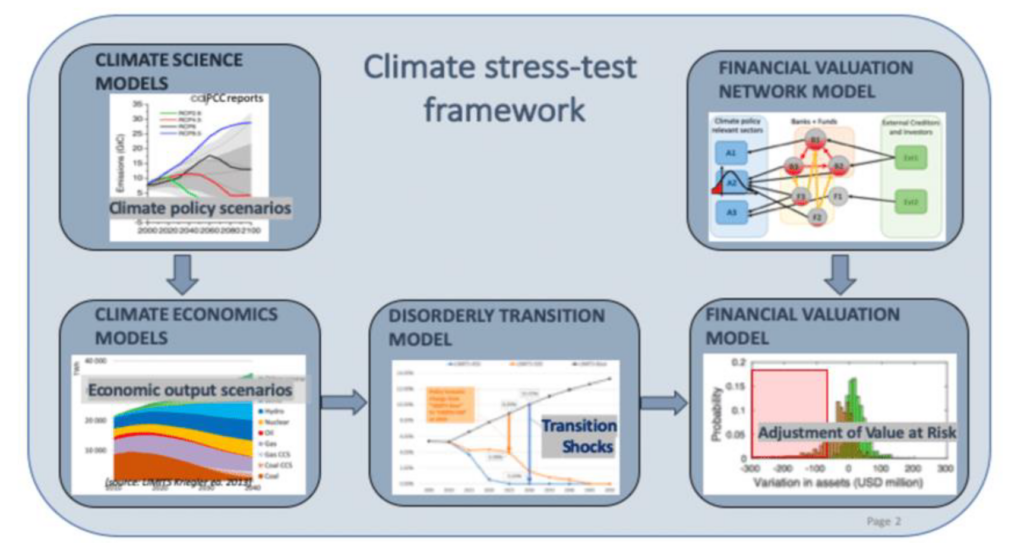

Systemic risk modeling is essential for central banks as financial systems grow more interconnected and vulnerable to sudden shocks. From market implied indicators to climate stress testing and… read more >>

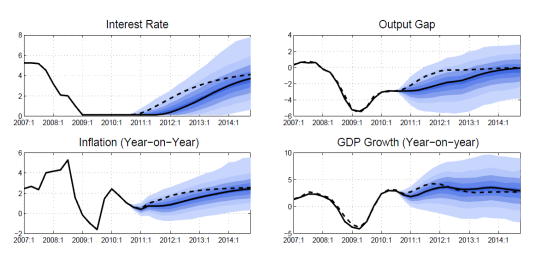

Nonlinear confidence bands help you quantify forecast uncertainty in DSGE models, but they can be slow to compute. At the MathWorks Finance Conference, Kadir Tanyeri (International Monetary Fund)… read more >>

Every MATLAB release opens the door to new capabilities, better performance, and tighter integration with the platforms your team already uses. With two major releases a year and over 800… read more >>

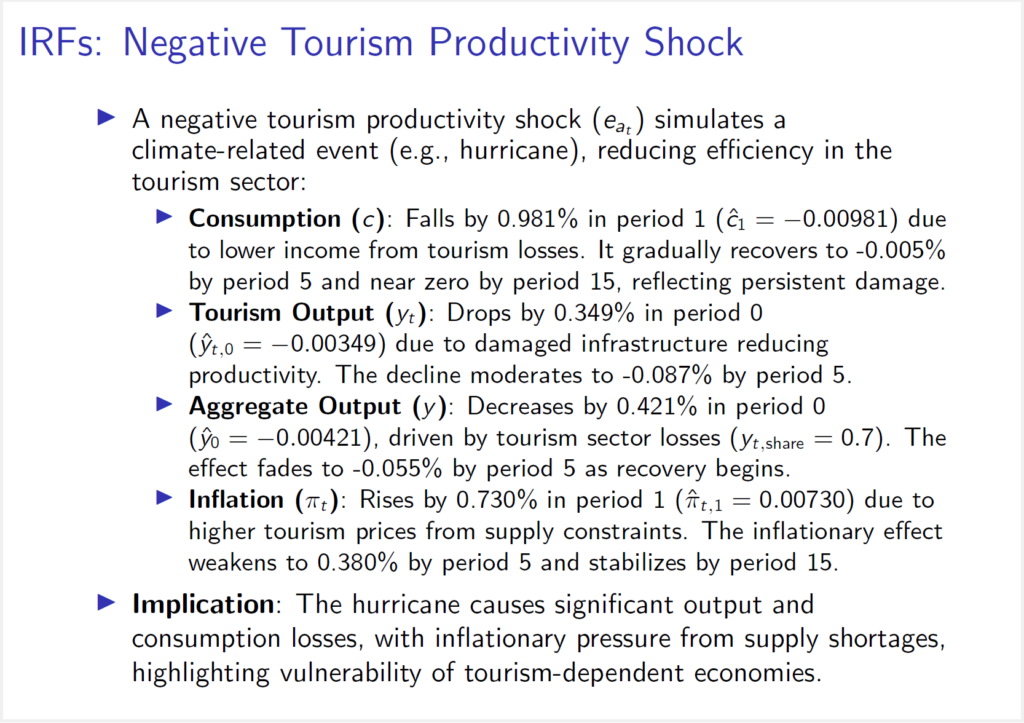

“It [MATLAB] was used in Dynare in order to promote the accuracy and the ease of generating this model.”— Allan Wright, Manager, Central Bank of the Bahamas

Watch the Full… read more >>