CRISK: A Market‑Based Framework for Quantifying Climate Risk in Banking

Effective risk management increasingly requires understanding how climate‑related factors can influence market valuations and balance‑sheet resilience. CRISK provides a transparent, market‑based framework for estimating the expected capital shortfall a bank might face under a climate stress scenario.

At the MathWorks Finance Conference, Michael Robbins (Columbia University) and Arpit Narain (MathWorks) discussed the CRISK framework, a practical, data‑driven approach to incorporate climate factors into systemic risk analysis.

What Is CRISK?

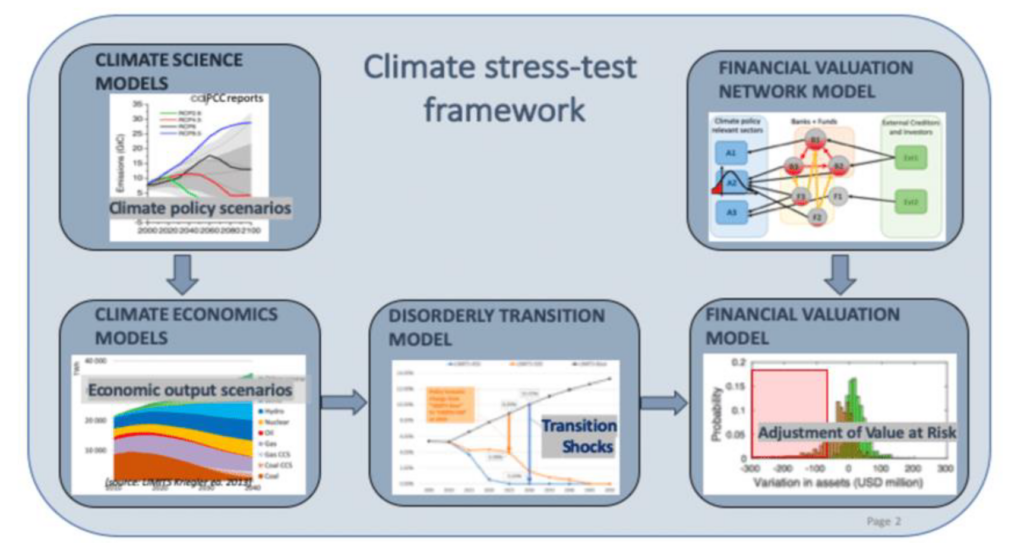

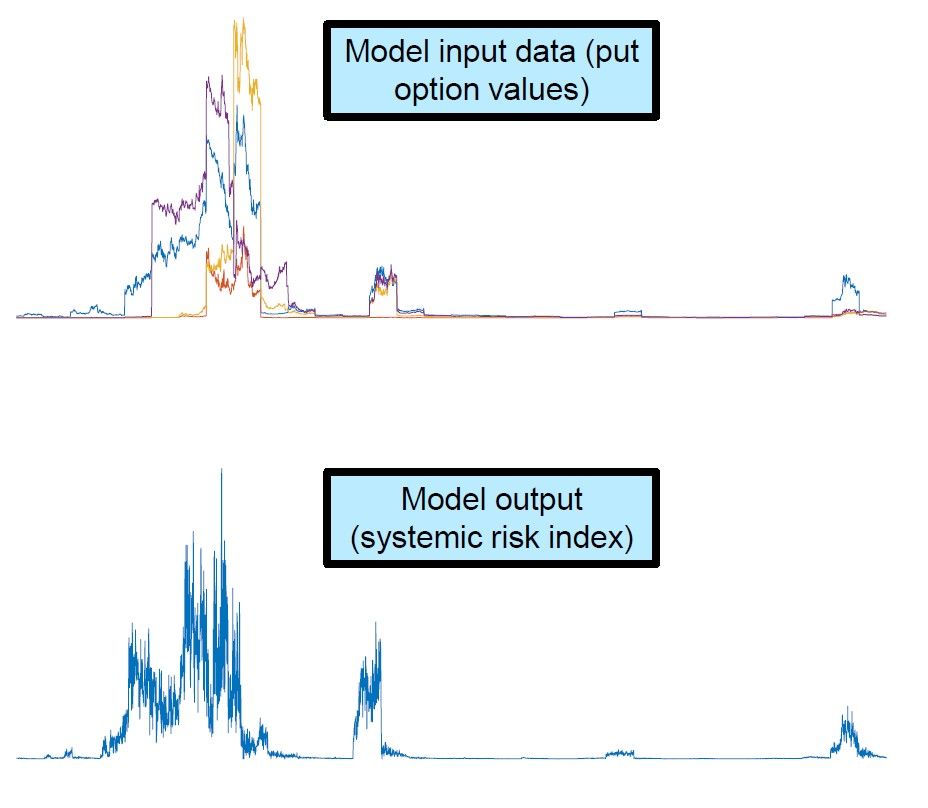

CRISK measures the expected capital shortfall a financial institution would face if a climate‑related systemic stress event were to occur.

The framework builds on research from the Federal Reserve Bank of New York and the academic work of Hyeyoon Jung, Robert Engle, and Richard Berner, whose contributions to volatility modelling and systemic risk underpin the methodology.

CRISK introduces two key components:

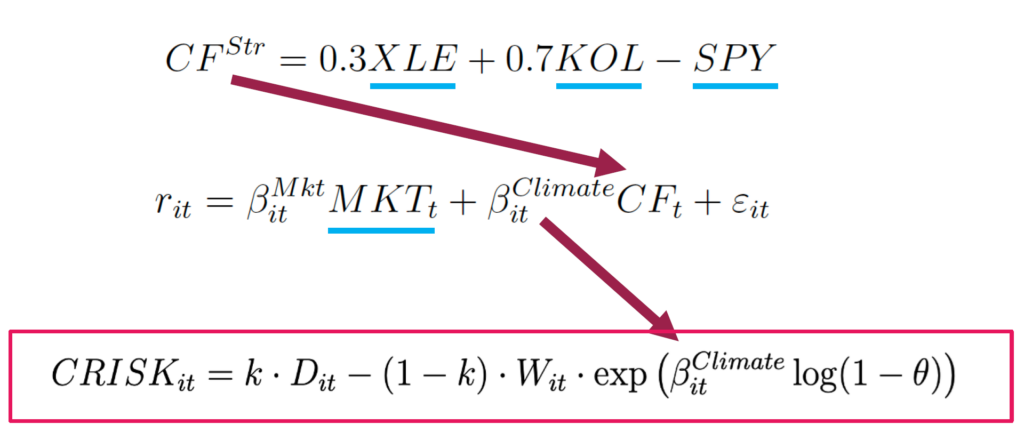

- Climate risk factors capturing transition or physical climate shocks

- Climate beta, quantifying a bank’s sensitivity to those factors

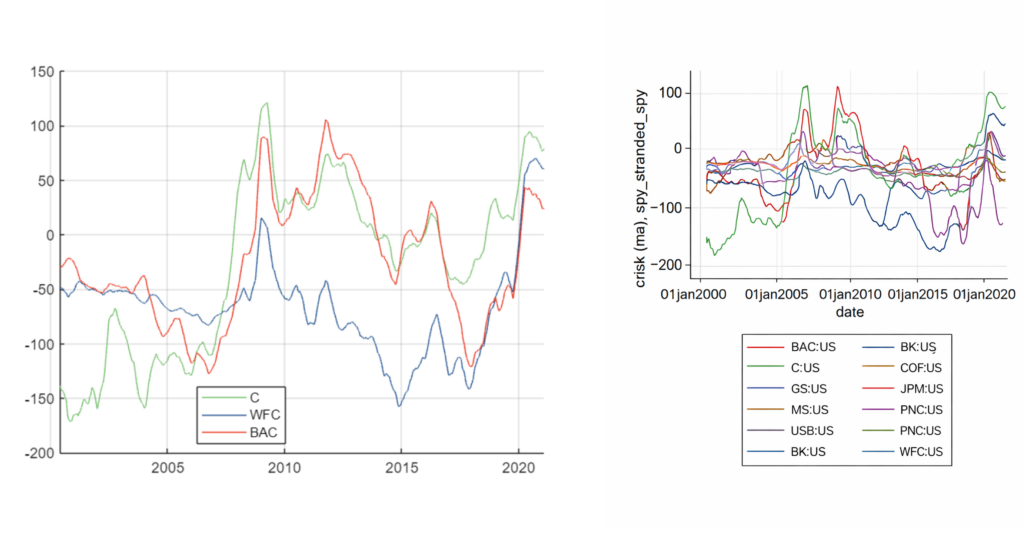

By linking climate betas to expected capital shortfall, CRISK provides a forward‑looking perspective on potential vulnerabilities in the banking system using only publicly available data.

Why CRISK Matters for Financial Institutions

Banks and supervisors increasingly need to quantify how climate scenarios affect capital adequacy. CRISK’s appeal lies in its:

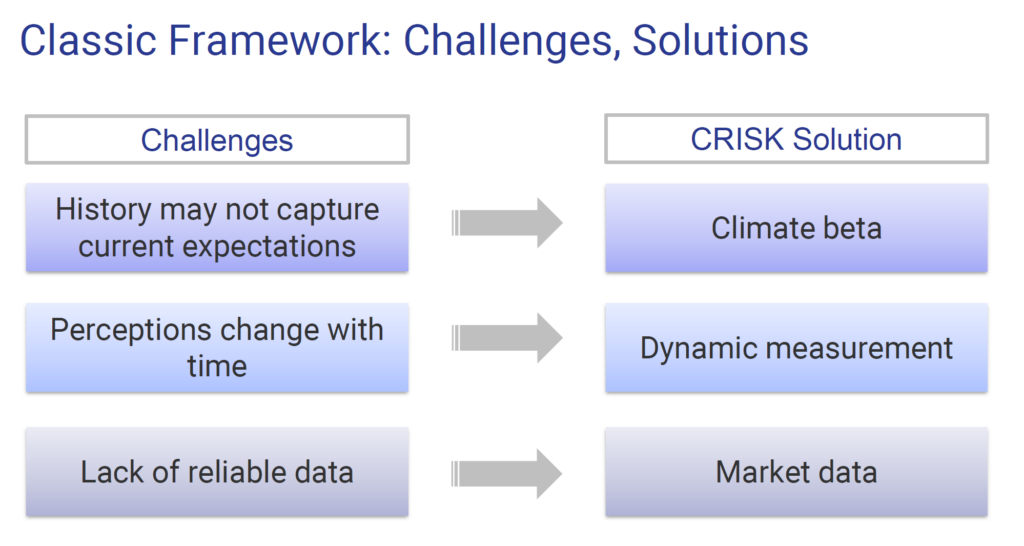

- Transparency — relies on publicly available equity, debt, and climate factor data

- Scalability — supports comparisons across firms and geographies

- Interpretability — produces a single, intuitive metric: expected capital shortfall

- Regulatory relevance — the method has already been replicated by a major Asian central bank

Implementing CRISK in MATLAB

The presentation highlighted how MATLAB supports a full‑stack implementation of CRISK, including estimation, scenario integration, and deployment.

Using MATLAB, institutions can:

- Build CRISK models tailored to local regulatory requirements

- Integrate climate factors from NGFS, national centres, or custom scenario sets

- Run large‑scale computations efficiently across portfolios

- Deploy models seamlessly to enterprise environments for reporting and auditability

This combination of transparency, rigor, and deployment readiness makes MATLAB a strong environment for central banks, supervisors, and large financial institutions implementing climate risk analytics.

Advancing Climate Risk Assessment

As climate‑related risks increasingly influence creditworthiness, asset valuations, and systemic resilience, CRISK enables institutions to:

- Quantify vulnerabilities to transition and physical risks

- Benchmark exposures across entities or jurisdictions

- Support supervisory dialogue and stress‑testing exercises

- Embed climate considerations directly into capital planning

CRISK represents a meaningful step toward a more data‑driven climate risk management ecosystem.

コメント

コメントを残すには、ここ をクリックして MathWorks アカウントにサインインするか新しい MathWorks アカウントを作成します。