Systemic Risk Modeling with MATLAB: Tools and Techniques for Central Banks

Systemic risk modeling is essential for central banks as financial systems grow more interconnected and vulnerable to sudden shocks. From market implied indicators to climate stress testing and network analytics, MATLAB provides a unified environment for developing models that help institutions identify vulnerabilities and prepare for emerging risks.

This overview highlights how central banks—including the Bank of England and the Austrian National Bank (OeNB)—use MATLAB to build scalable, transparent, and reproducible systemic risk frameworks.

What Is Systemic Risk Modeling?

Systemic risk modeling refers to the set of quantitative methods used to assess the stability of an entire financial system—not just individual institutions. Central banks rely on these models to:

- Detect early signs of stress

- Simulate crisis scenarios

- Understand contagion and network effects

- Strengthen supervisory and macroprudential decision‑making

MATLAB offers the computational performance, modeling flexibility, and workflow integration needed to support these high‑stakes analytical processes.

Market Implied Systemic Risk Indicators

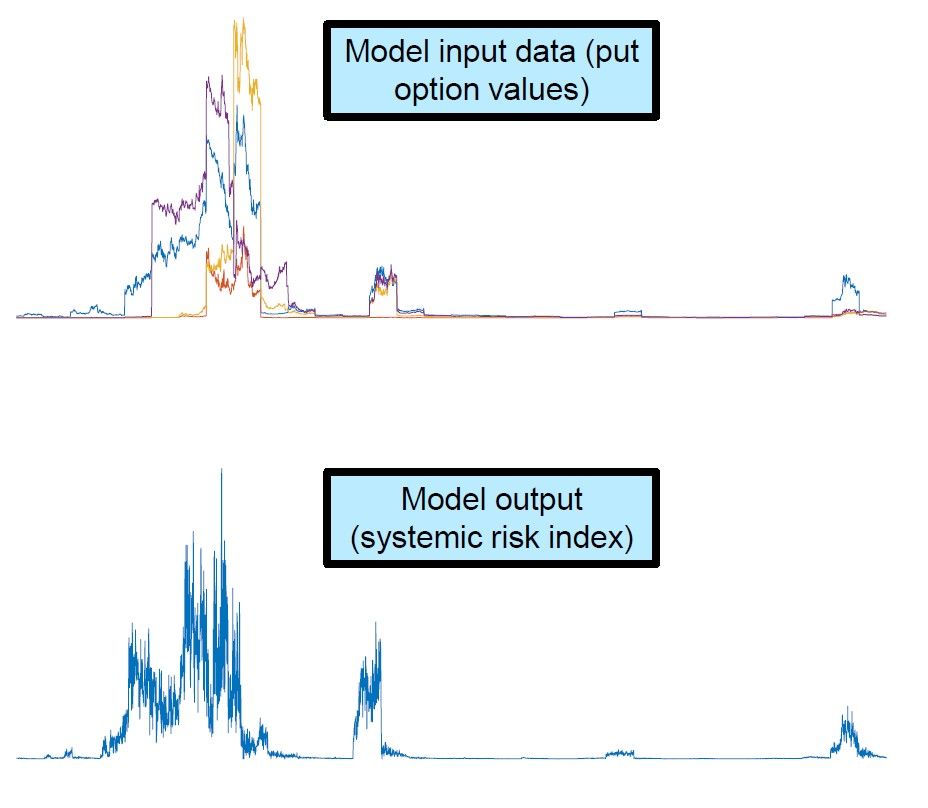

Early warning models based on put options

The Bank of England has used MATLAB to develop a systemic risk model based on put option values. These market implied indicators capture expectations of downside risk: when asset volatility rises, option values increase, signaling deteriorating conditions.

Key modeling components include:

- Autocorrelation functions for time‑dependent dynamics

- Extreme‑Value Theory (EVT) for tail‑event behavior

- T‑copula models to measure joint risk across banks

- Monte Carlo simulations for distributional and scenario analysis

By integrating these techniques, MATLAB enables analysts to build real‑time systemic risk dashboards and automate large‑scale simulations.

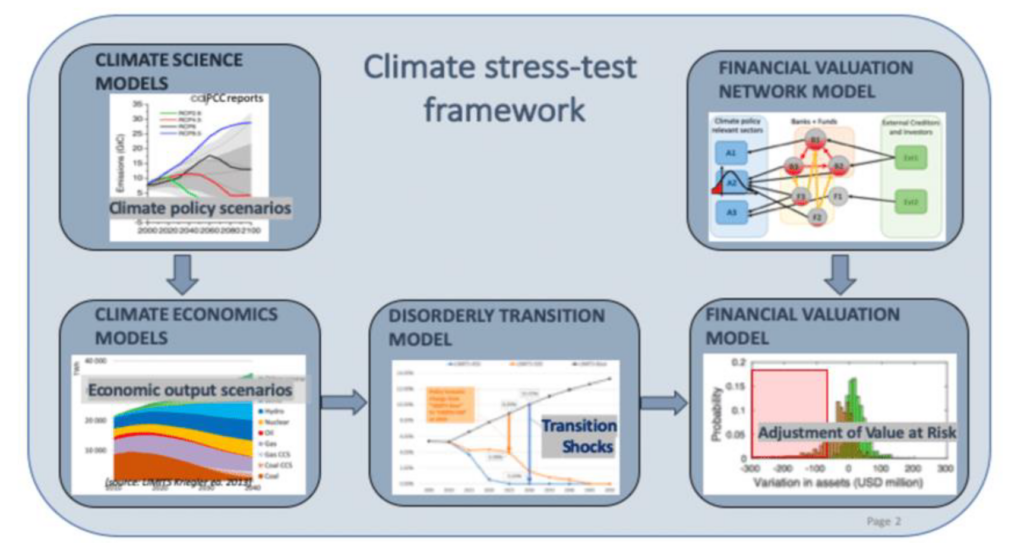

Climate Risk Stress Testing with MATLAB

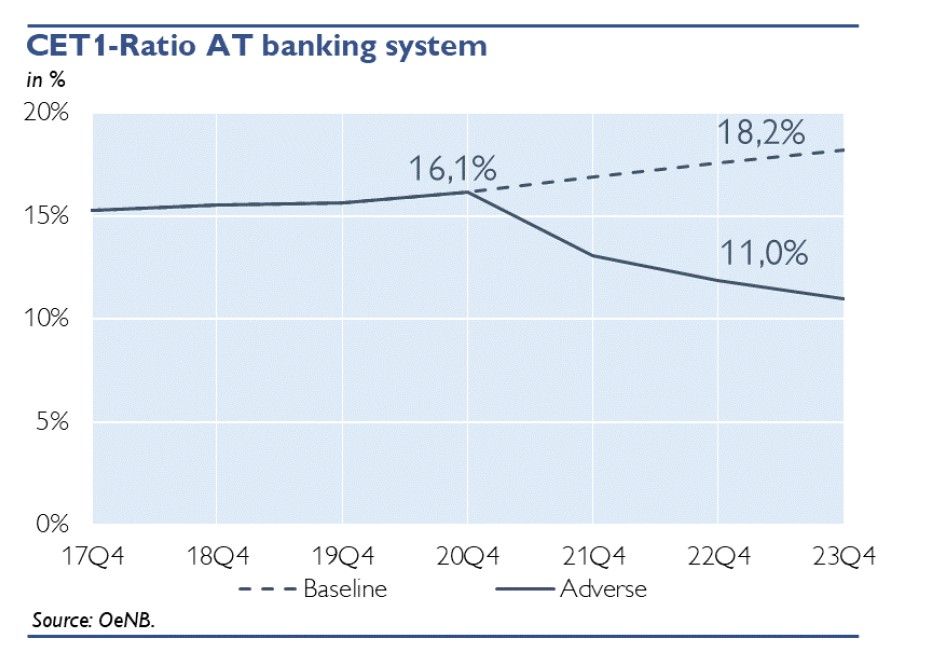

OeNB’s ARNIE framework

Climate risk has rapidly become a core component of systemic risk assessment. The Austrian National Bank (OeNB) developed its stress testing tool, ARNIE, using MATLAB to assess how carbon pricing, transition risks, and environmental shocks affect the banking sector.

Using MATLAB, the Austrian National Bank can:

- Process large climate‑related datasets

- Adjust credit risk models for climate scenarios

- Estimate changes in default probabilities and asset values

- Run multi‑scenario stress tests across the banking system

This adaptable framework supports both short‑term crisis analysis and long‑term climate scenario planning.

Watch a short overview of OeNB’s ARNIE climate risk stress-testing framework:

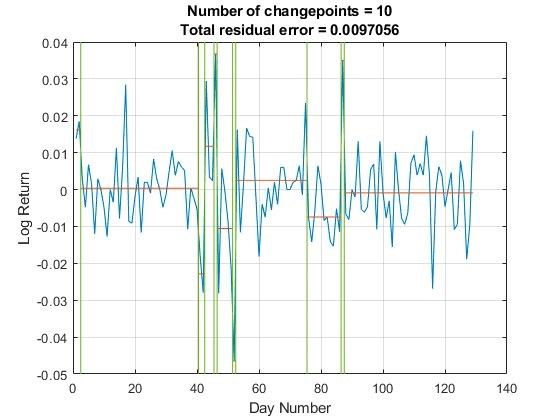

Jump‑Diffusion Models for Crisis‑Period Dynamics

Capturing sudden market jumps

Financial crises often involve abrupt, nonlinear market movements that traditional diffusion‑based models cannot capture. Central banks use jump‑diffusion models in MATLAB to better represent these dynamics.

MATLAB supports:

- Parameter estimation from historical time‑series

- Changepoint detection to identify structural breaks

- Simulation of tail‑event scenarios

- Integration with stress-testing and forecasting workflows

These models help risk teams anticipate how sudden shocks may propagate through markets and balance sheets.

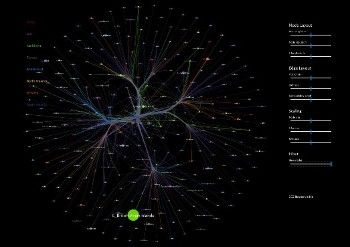

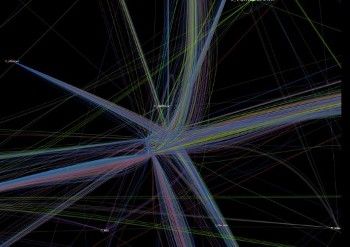

Network Analysis for Systemic Risk

Understanding interconnected financial systems

Systemic risk is often driven by the structure of the financial network itself. MATLAB graph analytics capabilities allow central banks to map relationships between institutions and uncover hidden vulnerabilities.

Typical workflows include:

- Building exposure networks

- Identifying systemically important institutions

- Modeling contagion pathways

- Simulating cascading defaults or liquidity shocks

Network visualization and metrics give policymakers deeper insight into how risks spread across the financial system.

Financial network visualization showing interdependencies between global banking institutions, modeled using MATLAB

Why Central Banks Choose MATLAB for Systemic Risk Modeling

Across all these use cases, MATLAB offers advantages that align directly with supervisory needs:

- Integrated workflow: data ingestion, modeling, simulation, and reporting in one environment

- Scalability: efficient execution of large‑scale Monte Carlo, network models, and climate scenarios

- Flexibility: easy adaptation as regulatory frameworks evolve

- Transparency: clear, reproducible modeling pipelines crucial for supervisory review

- Deployment: options for integration with IT infrastructures, cloud computing, and web apps

Conclusion: Building More Resilient Financial Systems With MATLAB

Systemic risk modeling is a multidisciplinary challenge involving finance, statistics, climate science, and network analysis. MATLAB equips central banks with the tools they need to integrate these components into transparent, scalable, and adaptable modeling frameworks. From market implied indicators to climate stress tests and network contagion models, MATLAB helps institutions strengthen financial stability and build resilience against future shocks.

Comments

To leave a comment, please click here to sign in to your MathWorks Account or create a new one.