GDP Nowcasting with MATLAB

What is GDP Nowcasting?

Imagine trying to drive a car while only getting speed updates every three months. That’s kind of what it’s like for central banks relying solely on quarterly GDP data to make policy decisions. By the time the numbers come out, the economy might already be in a different state.

GDP nowcasting is a way to estimate GDP growth in real time using high-frequency data like monthly employment figures, industrial production, credit card transactions, and even news sentiment. It’s like having a live dashboard for the economy instead of waiting for the quarterly report card.

For central banks, investors, and policymakers, nowcasting is beneficial because it can:

- Detect economic shifts before they appear in official data

- Inform monetary and financial stability decisions with up-to-date information

- Fill gaps between quarterly releases and revised GDP figures

MATLAB has a number of tools to help central bankers build these nowcasting models, from econometrics to machine learning and real-time data handling.

How Different Institutions Are Nowcasting GDP

Around the world, economists have built nowcasting models using different techniques—some classic, some cutting-edge. Here’s a quick tour of the most popular approaches:

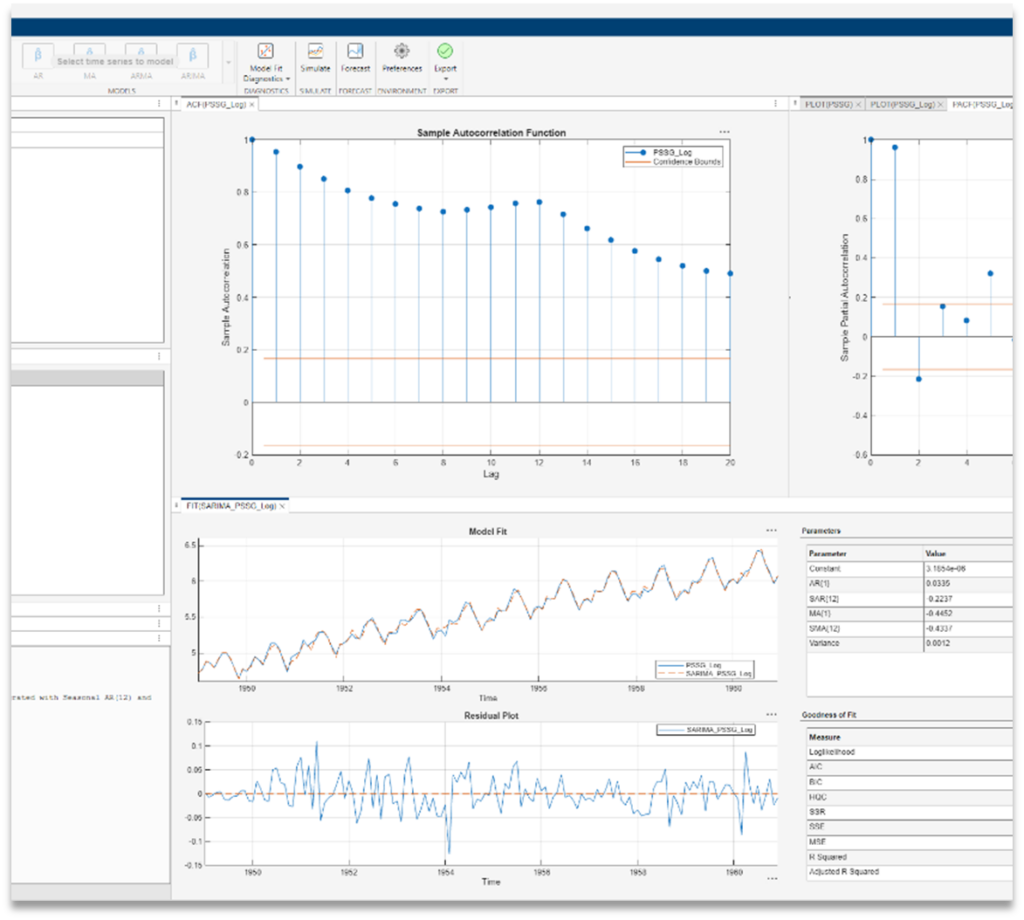

Dynamic Factor Models (DFMs)

DFMs are the go-to for many central banks because they handle large datasets effortlessly. The idea is simple: instead of tracking hundreds of economic indicators separately, DFMs extract a few key underlying trends (factors) that drive GDP. Since GDP is quarterly but other data (like employment or industrial production) is monthly, DFMs use Kalman filters to blend everything smoothly.

Bridge Equations

Bridge equations directly link high-frequency indicators (like retail sales or PMIs) to GDP using regression. No latent factors—just a straightforward model that says, “If industrial production grew this month, GDP probably grew this quarter.” Some versions use MIDAS (Mixed Data Sampling) regression to handle mismatched data frequencies.

Machine Learning (ML)

ML models (like random forests, neural networks, or LSTMs) are gaining traction because they can detect complex patterns in messy, real-world data. Instead of assuming linear relationships, they learn from history—including unconventional data like credit card transactions or shipping logs. The catch? They need tons of data and can be “black boxes,” but when tuned right, they often outperform traditional models.

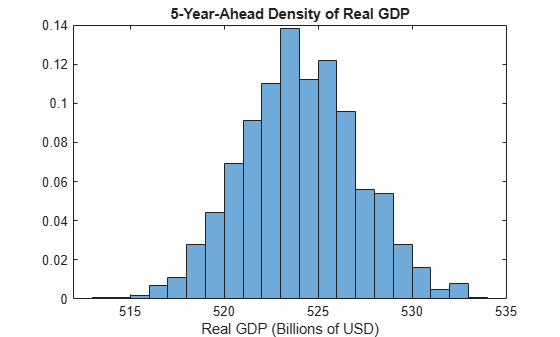

Bayesian VARs (BVARs)

For countries with limited GDP history, BVARs are a lifesaver. They work like regular VARs but let economists inject expert knowledge (priors) to fill in the gaps. For example: “GDP growth tends to persist, so let’s nudge the model in that direction.” The Bayesian approach keeps the model from overfitting, making it great for emerging markets or fast-changing economies.

Text Analytics

Some of the most innovative models now use news sentiment, earnings calls, or social media to predict GDP. By scraping headlines and scoring tone (positive/negative), economists can gauge economic momentum in real time. It’s not a standalone solution, but when combined with traditional data, it adds a powerful forward-looking signal.

Why use MATLAB for Nowcasting?

- Easy data integration: MATLAB connects to Bloomberg, FRED, Eurostat, and a number of other data feeds through the Datafeed Toolbox

- Mix and match models: Start with a simple regression, then add machine learning or Bayesian tweaks with the Statistics and Machine Learning Toolbox and Econometrics Toolbox

- Build real-time dashboards: Deploy your nowcast as a web app or integrate it into a policy dashboard using App Designer and the Web App Server

- Backtesting functionality: See how your model would have performed in past crises before trusting it with real decisions using the backtesting framework

Want to Build Your Own Nowcasting Model?

If your team is thinking about setting up (or upgrading) a GDP nowcasting system, MathWorks can help with:

- Custom model development (DFMs, ML, hybrid approaches)

- Real-time data pipeline integration

- Performance benchmarking & backtesting

- Category:

- Econometrics

Comments

To leave a comment, please click here to sign in to your MathWorks Account or create a new one.