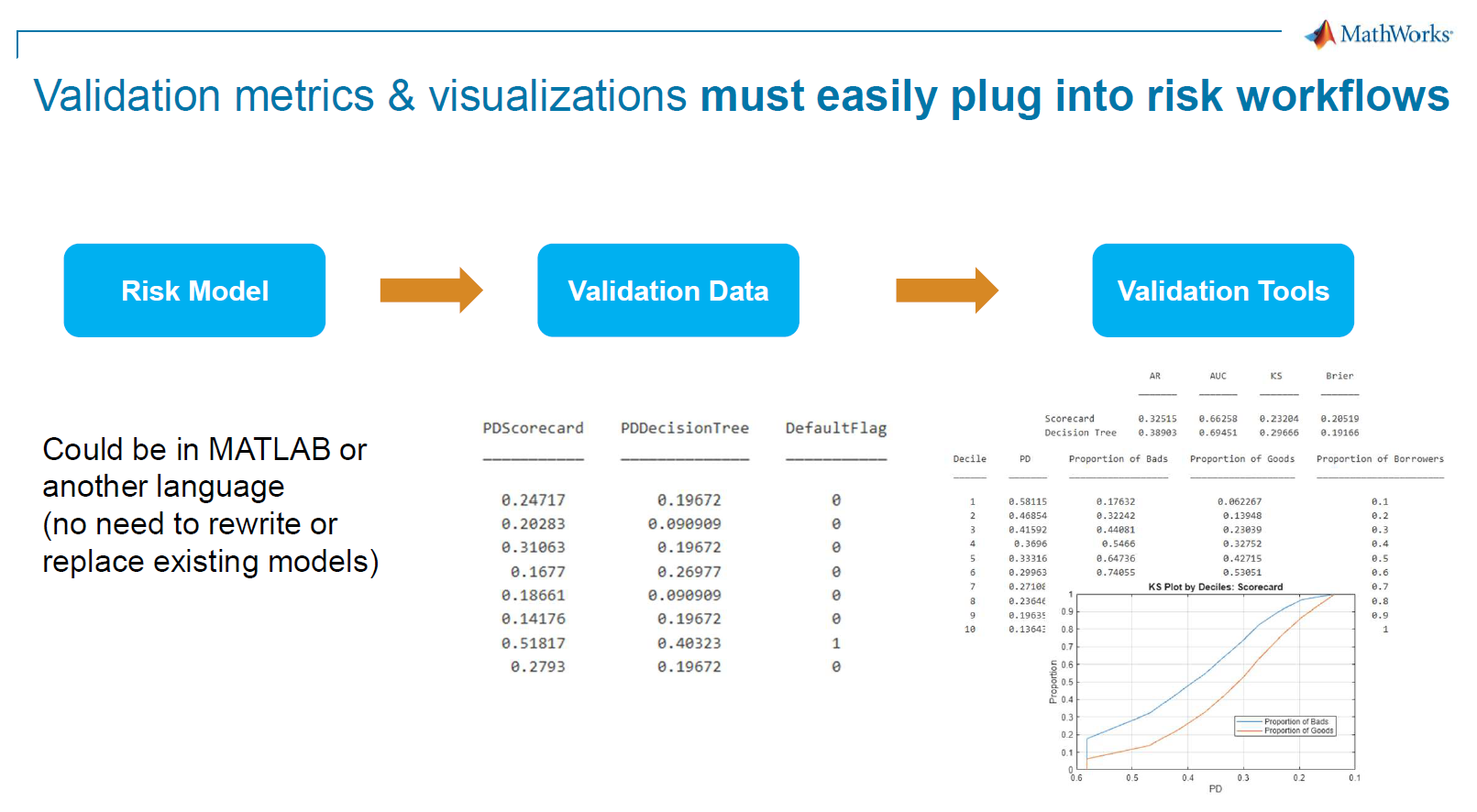

In this technical session, Valerio Sperandeo, Senior Application Engineer, demonstrated how MATLAB can support financial institutions in building robust, transparent, and scalable risk models aligned… read more >>

In this technical session, Valerio Sperandeo, Senior Application Engineer, demonstrated how MATLAB can support financial institutions in building robust, transparent, and scalable risk models aligned… read more >>

Dynamic Stochastic General Equilibrium (DSGE) models are essential tools for policy analysis and forecasting, but estimation runs often exceed 24 hours—particularly for large-scale models or Bayesian… read more >>

Summary

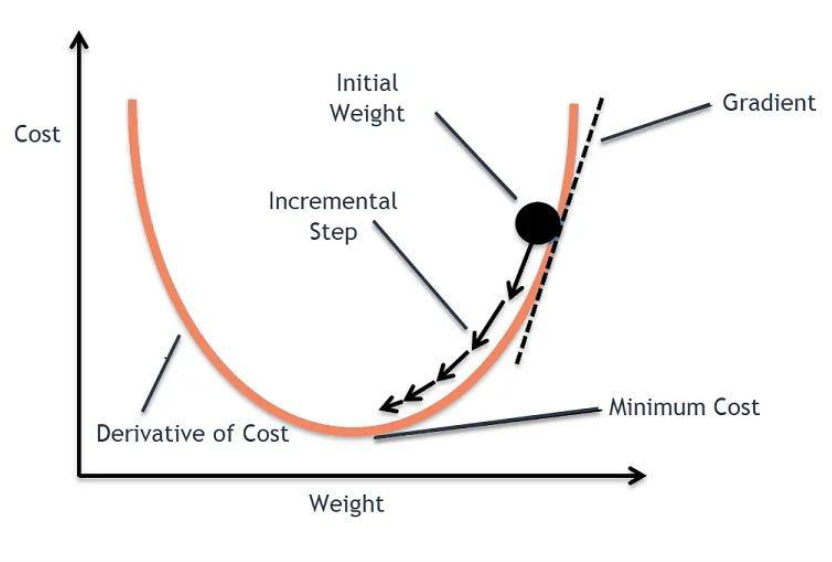

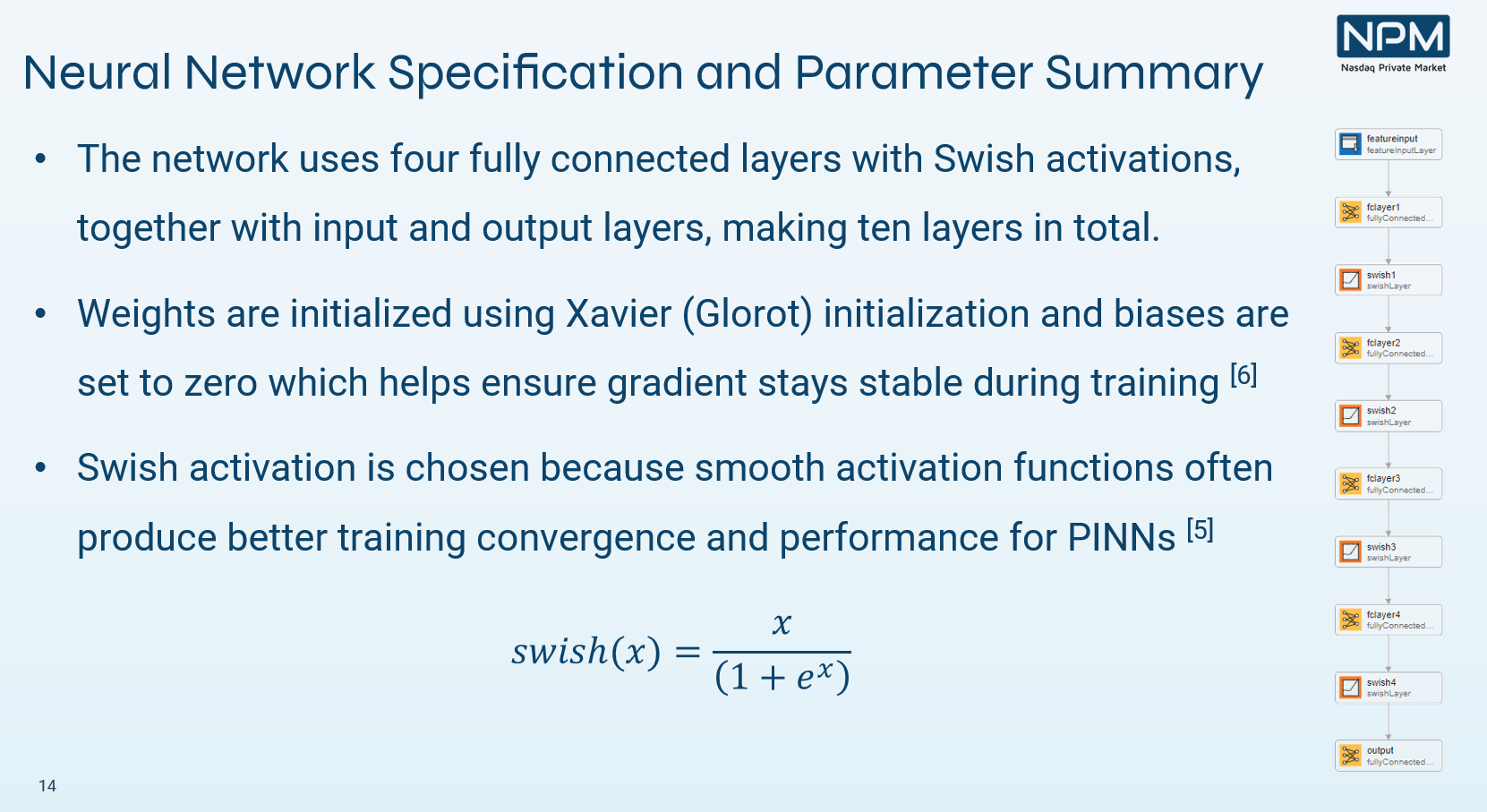

Nasdaq Private Market (NPM) used MATLAB® to prototype and scale physics‑informed neural networks (PINNs) that price Special Purpose Vehicles (SPVs) with embedded carried interest and… read more >>

The 2025 MathWorks Finance Conference brought together quants, economists, financial modelers and researchers to explore how MATLAB is shaping the future of finance. Across two days, speakers shared… read more >>

The following post is from Yuchen Dong, Senior Finance Application Engineer at MathWorks.

The example featured in the blog can be found on GitHub here.

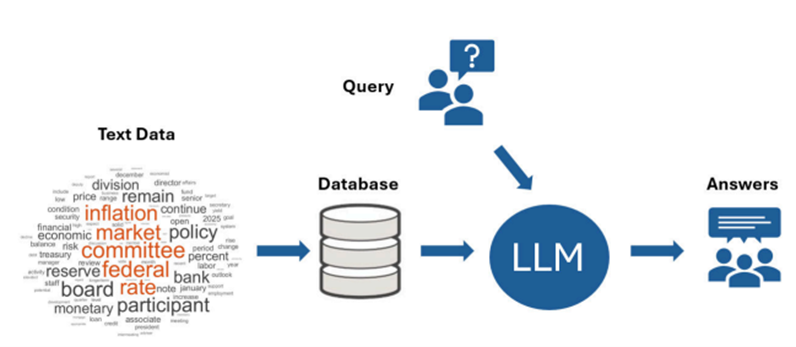

Retrieval-Augmented Generation (RAG) has… read more >>

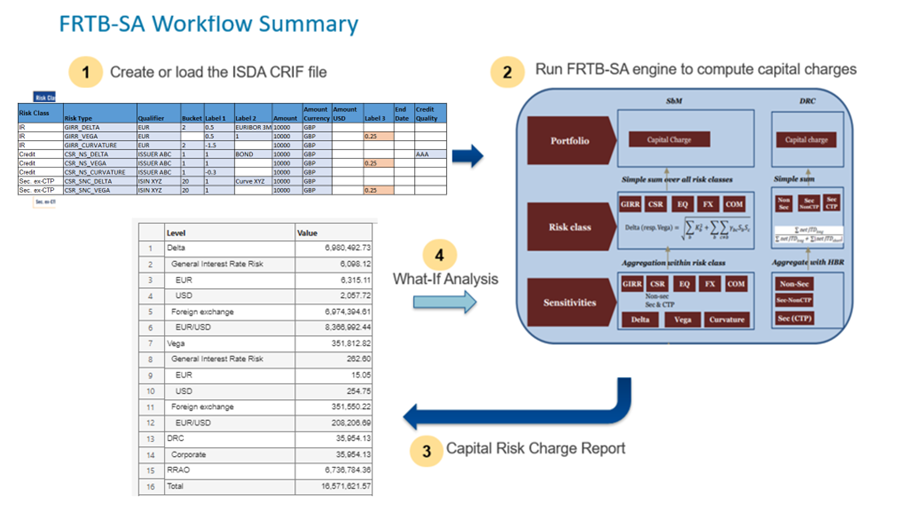

The Fundamental Review of the Trading Book (FRTB) is reshaping how banks measure and manage market risk. Beyond replacing Value at Risk (VaR) with Expected Shortfall (ES) to better capture tail risk… read more >>

If you work with macro, markets, or policy analysis, chances are you touch FRED®—the Federal Reserve Economic Data service. The Datafeed Toolbox gives you a first-class, native connector to FRED that… read more >>

We recently hosted a technical webinar focused on analyzing the financial risks of wildfires. Akshay Paul and Yuchen Dong from the MathWorks finance team presented how MATLAB can support financial… read more >>

The following post is from Yuchen Dong, Senior Financial Application Engineer at MathWorks.

Financial institutions forecast GDP to set capital buffers and plan stress-testing scenarios. Using MATLAB®… read more >>

What is GDP Nowcasting?

Imagine trying to drive a car while only getting speed updates every three months. That’s kind of what it’s like for central banks relying solely on quarterly GDP data to make… read more >>