Expert Contributor: Dr. Yuchen Dong

Yuchen is a Senior Application Engineer at MathWorks focusing on customers in the financial services industry. His focus areas are financial instruments,… 더 읽어보기 >>

Expert Contributor: Dr. Yuchen Dong

Yuchen is a Senior Application Engineer at MathWorks focusing on customers in the financial services industry. His focus areas are financial instruments,… 더 읽어보기 >>

Summary

Nasdaq Private Market (NPM) used MATLAB® to prototype and scale physics‑informed neural networks (PINNs) that price Special Purpose Vehicles (SPVs) with embedded carried interest and… 더 읽어보기 >>

The 2025 MathWorks Finance Conference brought together quants, economists, financial modelers and researchers to explore how MATLAB is shaping the future of finance. Across two days, speakers shared… 더 읽어보기 >>

The following post is from Yuchen Dong, Senior Finance Application Engineer at MathWorks.

The example featured in the blog can be found on GitHub here.

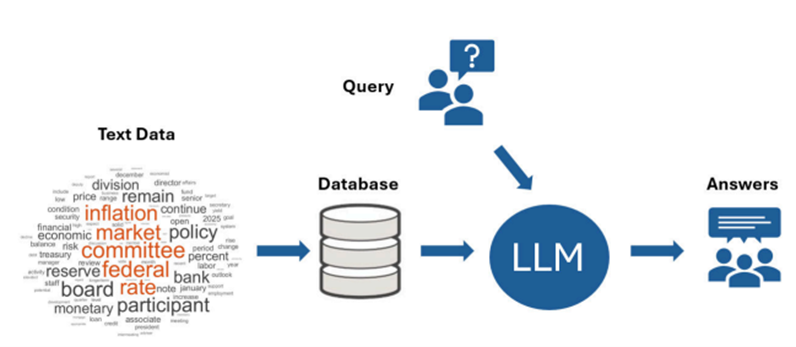

Retrieval-Augmented Generation (RAG) has… 더 읽어보기 >>

The following post is from Yuchen Dong, Senior Financial Application Engineer at MathWorks.

Financial institutions forecast GDP to set capital buffers and plan stress-testing scenarios. Using MATLAB®… 더 읽어보기 >>

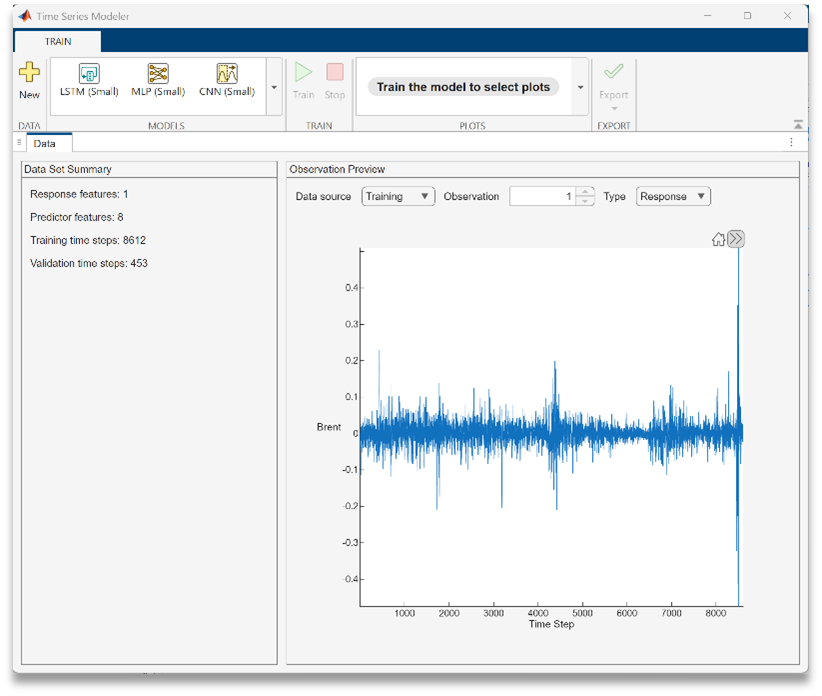

The following post is from Jue Liu from Columbia University and Yuchen Dong from MathWorks.

The example featured in the blog can be found on GitHub here.

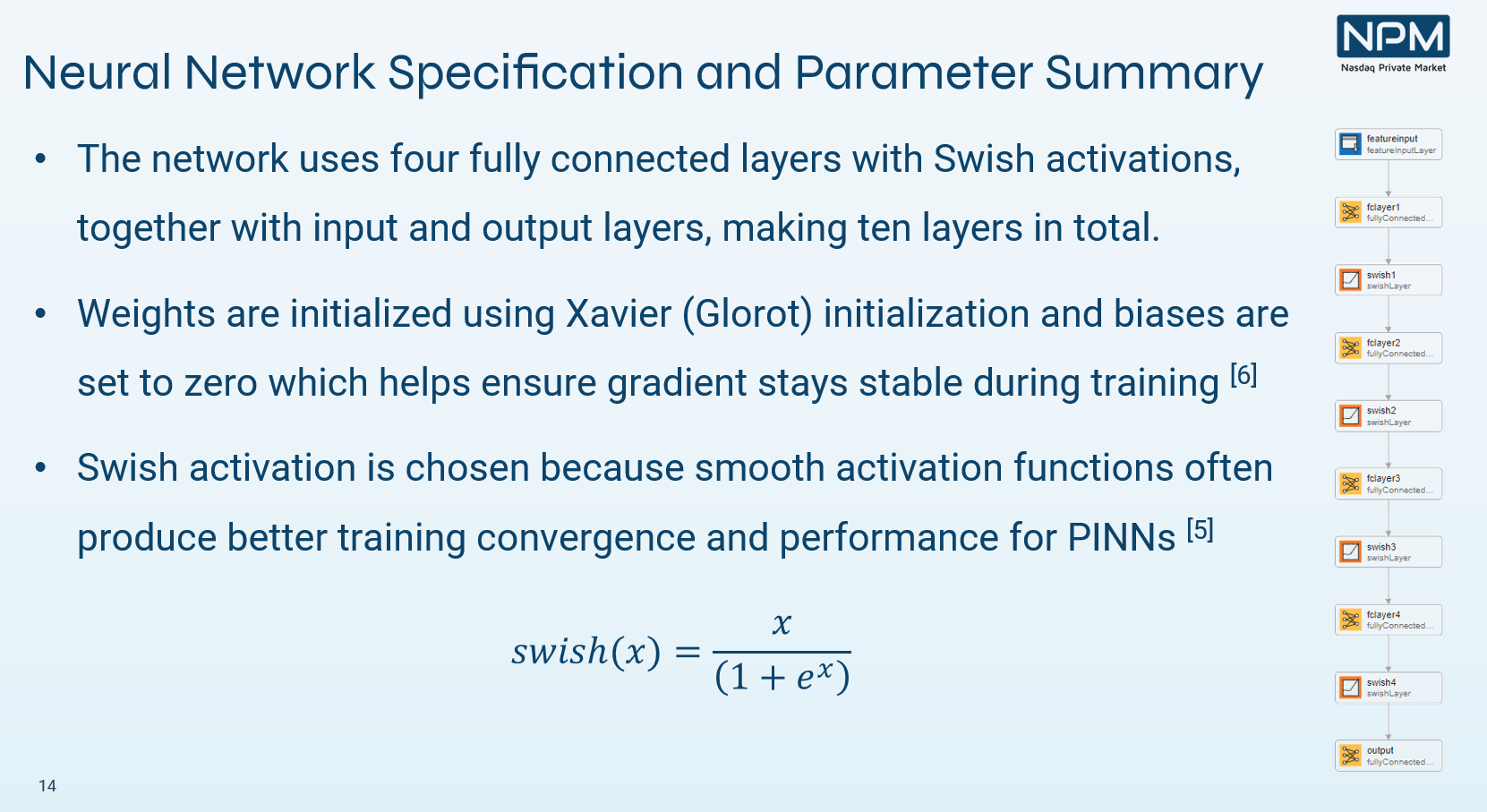

View the Physics-Informed Neural Networks… 더 읽어보기 >>

We are proud to announce that MathWorks has been ranked second overall in the inaugural Chartis RiskTech AI 50, an independent and highly respected evaluation of the top 50 providers of AI-driven… 더 읽어보기 >>

The following blog was written by Adam Peters, Software Engineer at Mathworks.

Download the code for this example from Github here

Overview:

Financial trading optimization involves developing a… 더 읽어보기 >>

The following blog was written by Sara Galante, Senior Finance Application Engineer at Mathworks.

MathWorks now has a curated selection of quant finance resources using MATLAB . Whether you’re… 더 읽어보기 >>

The following blog was written by Owen Lloyd , a Penn State graduate who recently join the MathWorks Engineering Development program.

The code used to develop this example can be found on GitHub… 더 읽어보기 >>