Cleve’s Corner: Cleve Moler on Mathematics and Computing

Cleve’s Corner: Cleve Moler on Mathematics and Computing The MATLAB Blog

The MATLAB Blog Guy on Simulink

Guy on Simulink MATLAB Community

MATLAB Community Artificial Intelligence

Artificial Intelligence Developer Zone

Developer Zone Stuart’s MATLAB Videos

Stuart’s MATLAB Videos Behind the Headlines

Behind the Headlines File Exchange Pick of the Week

File Exchange Pick of the Week Hans on IoT

Hans on IoT Student Lounge

Student Lounge MATLAB ユーザーコミュニティー

MATLAB ユーザーコミュニティー Startups, Accelerators, & Entrepreneurs

Startups, Accelerators, & Entrepreneurs Autonomous Systems

Autonomous Systems Quantitative Finance

Quantitative Finance MATLAB Graphics and App Building

MATLAB Graphics and App Building

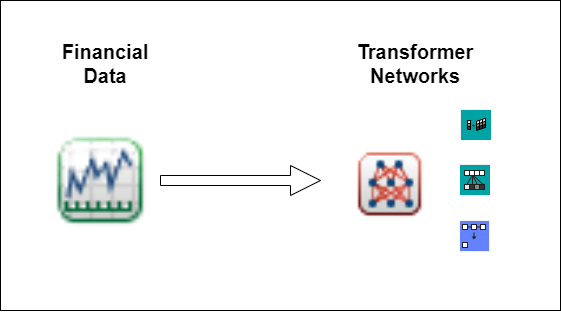

The following blog was written by Adam Peters, Software Engineer at Mathworks.

Download the code for this example from Github here

Overview:

Financial trading optimization involves developing a… read more >>

Derivative of state ‘1’ in block ‘X/Y/Integrator’ at time 0.55 is not finite

Inspiring Connections during the “Women at MathWorks” Breakfast Mixer

Streamlining the Medical Imaging Software Development Lifecycle

Three favorites from TIME Magazine’s “Best Innovations of 2023”

New ThingSpeak IoT Examples and Curriculum Module: Hardware Connectivity in Action

Startup Shorts: Flux Marine Redefines Marine Propulsion Through Electrification

Developing Inertial Navigation Systems with MATLAB – From Sensor Simulation to Sensor Fusion

Deep Learning in Quantitative Finance: Multiagent Reinforcement Learning for Financial Trading

Animating Science: Creating Time-Sensitive Animations with MATLAB

The following blog was written by Adam Peters, Software Engineer at Mathworks.

Download the code for this example from Github here

Overview:

Financial trading optimization involves developing a… read more >>

Background

In the rapidly evolving landscape of financial risk management, addressing climate risk has emerged as a critical imperative. MathWorks, in collaboration with Marcus Evans, recently… read more >>

The following blog was written by Sara Galante, Senior Finance Application Engineer at Mathworks.

MathWorks has a new application to implement backtesting strategies available on GitHub. This custom… read more >>

The following blog was written by Sara Galante, Senior Finance Application Engineer at Mathworks.

MathWorks now has a curated selection of quant finance resources using MATLAB . Whether you’re… read more >>

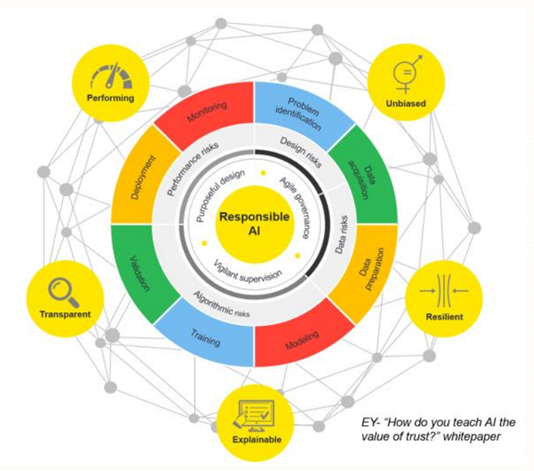

MathWorks recently hosted a webinar on Model Monitoring and Drift Detection, where Paul Peeling presented strategies for maintaining the health and fairness of deployed models using the MathWorks… read more >>

The following blog was written by Owen Lloyd , a Penn State graduate who recently join the MathWorks Engineering Development program.

The code used to develop this example can be found on GitHub… read more >>

The following blog was written by Arpit Narain from the MathWorks Finance team.

1. Introduction

In today’s financial landscape, climate risk has taken center stage, demanding the attention of… read more >>

The following blog was written by Sara Galante, Senior Finance Application Engineer at Mathworks.

The code used to develop this example can be found on GitHub here: Managing Asset Allocation with… read more >>

The following blog was written by Leslie Zhang, a Northeastern graduate who recently joined MathWorks Engineering Development program. This post aims to highlight the collaboration opportunities… read more >>

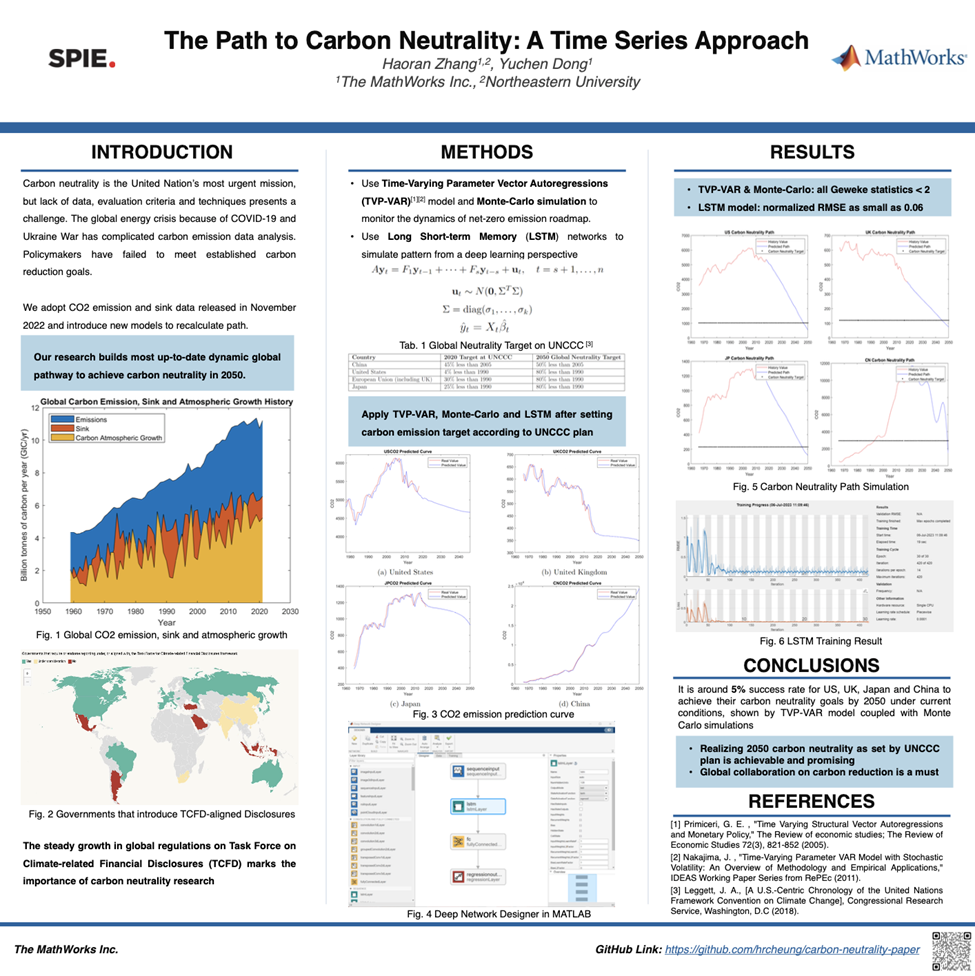

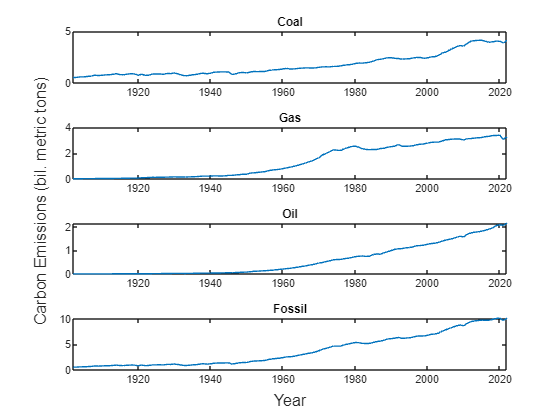

The following post is from Hang Qian, Software Developer on the Econometrics Toolbox Team.

Global carbon emissions have increased dramatically since 1901. However, the annual growth rates were… read more >>

These postings are the author's and don't necessarily represent the opinions of MathWorks.