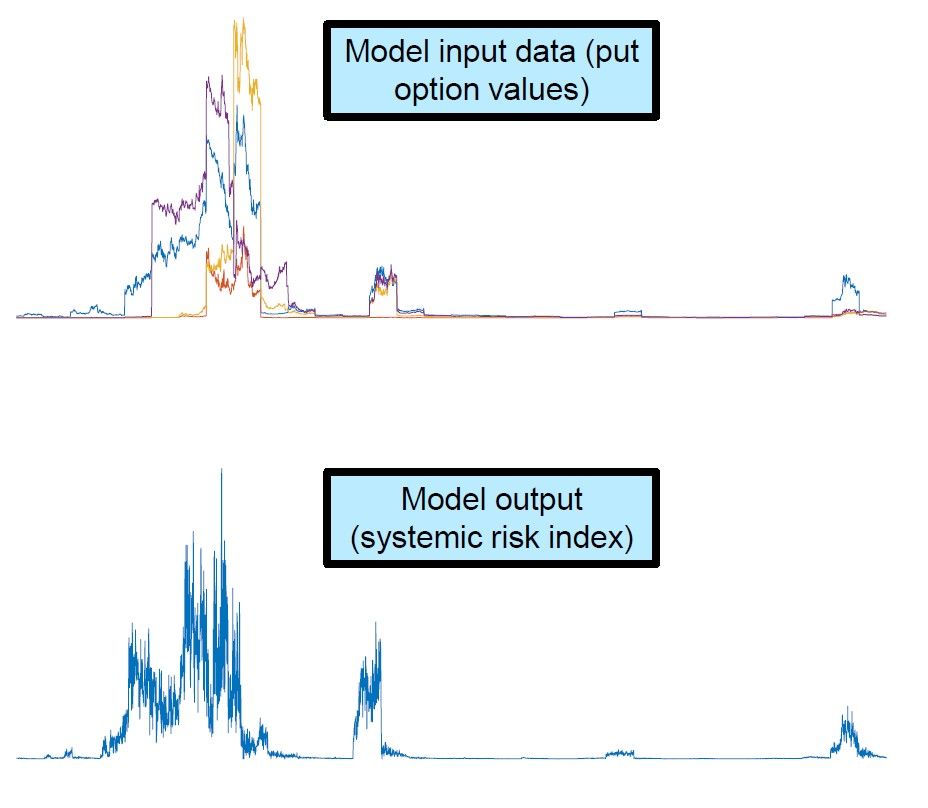

Systemic risk modeling is essential for central banks as financial systems grow more interconnected and vulnerable to sudden shocks. From market implied indicators to climate stress testing and… 更多内容 >>

Systemic risk modeling is essential for central banks as financial systems grow more interconnected and vulnerable to sudden shocks. From market implied indicators to climate stress testing and… 更多内容 >>

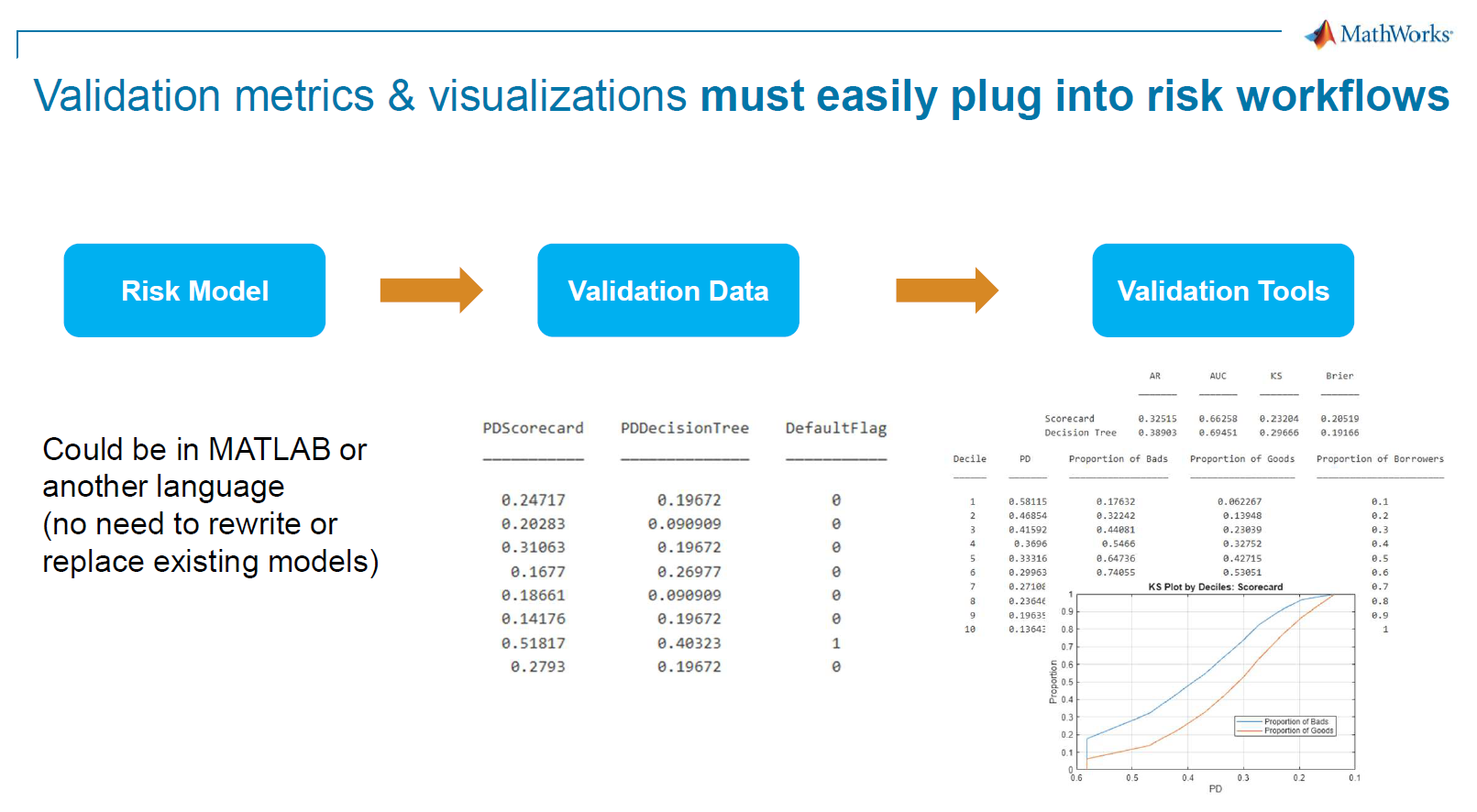

In this technical session, Valerio Sperandeo, Senior Application Engineer, demonstrated how MATLAB can support financial institutions in building robust, transparent, and scalable risk models aligned… 更多内容 >>

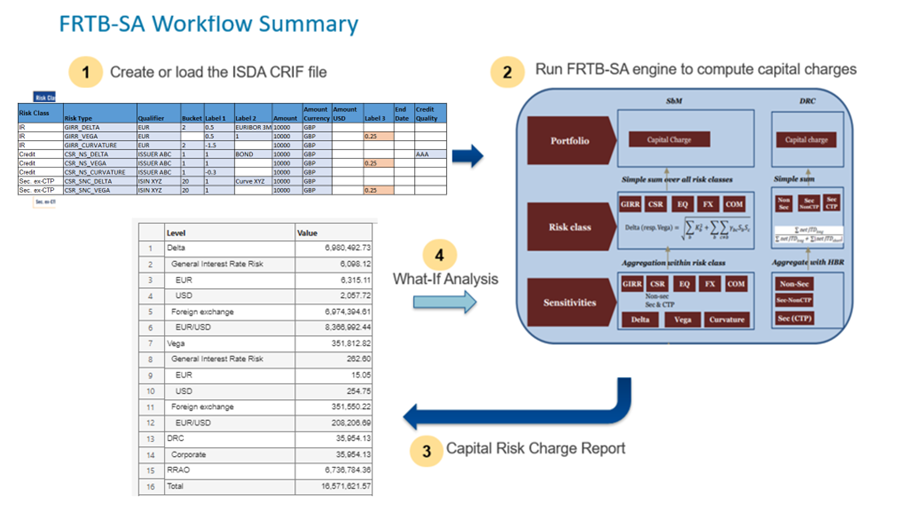

The Fundamental Review of the Trading Book (FRTB) is reshaping how banks measure and manage market risk. Beyond replacing Value at Risk (VaR) with Expected Shortfall (ES) to better capture tail risk… 更多内容 >>

The following blog was written by Sara Galante, Senior Finance Application Engineer at Mathworks.

MathWorks has a new application to implement backtesting strategies available on GitHub. This custom… 更多内容 >>