A Practical Guide to Git in MATLAB

The Problem You Already Have

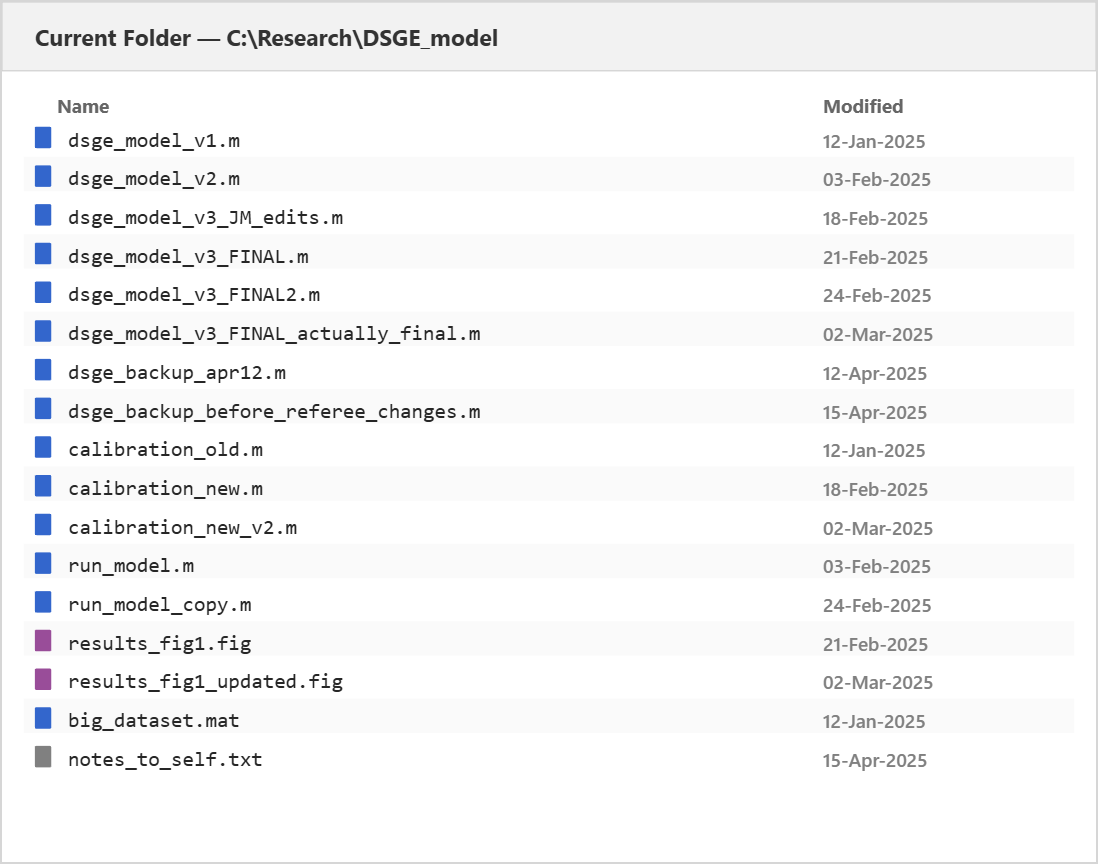

You know the folder. Somewhere on your machine there is a directory that looks like this:

A familiar sight: version history encoded… read more >>

A Practical Guide to Git in MATLAB

The Problem You Already Have

You know the folder. Somewhere on your machine there is a directory that looks like this:

A familiar sight: version history encoded… read more >>

Economists often keep years of work in EViews workfiles: macroeconomic series, model estimates, and curated panel data. The MATLAB Reader for EViews Workfile reads .wf1 and .wf2 files into MATLAB,… read more >>

Expert Contributor: Dr. Eduard Benet Cerdà

Edu is a Senior Application Engineer at MathWorks advising customers in the development and deployment of financial applications. His focus… read more >>

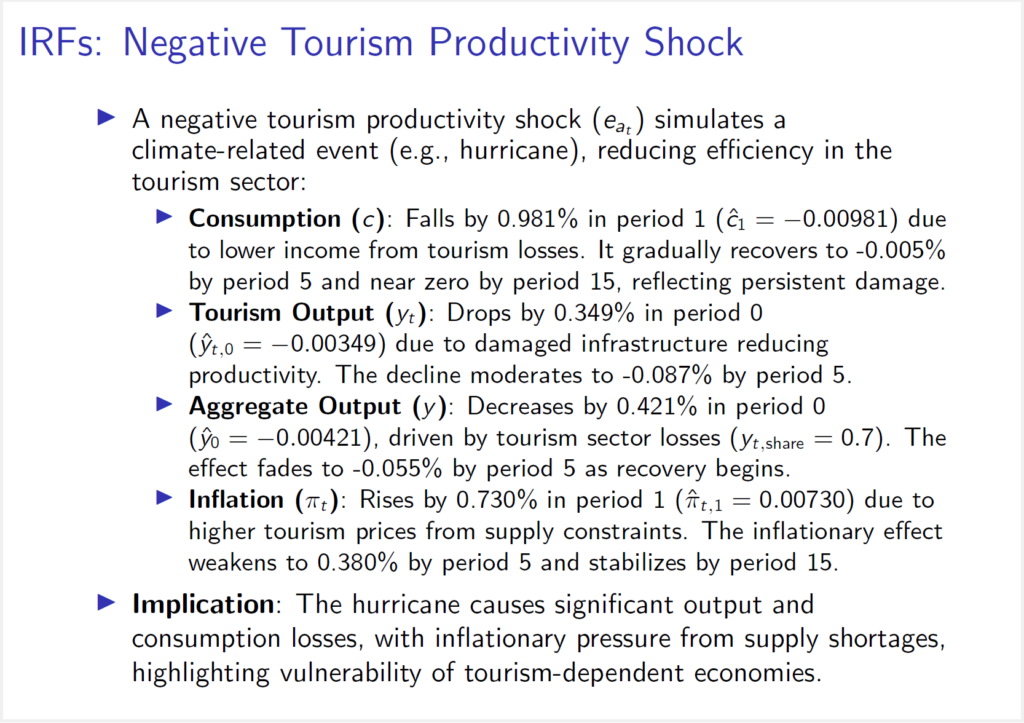

R2026a covers a lot of ground for economists—Bayesian state-space estimation, macro-scale forecasting, climate and physical risk mapping, symbolic dynamics, and AI-assisted model review, among… read more >>

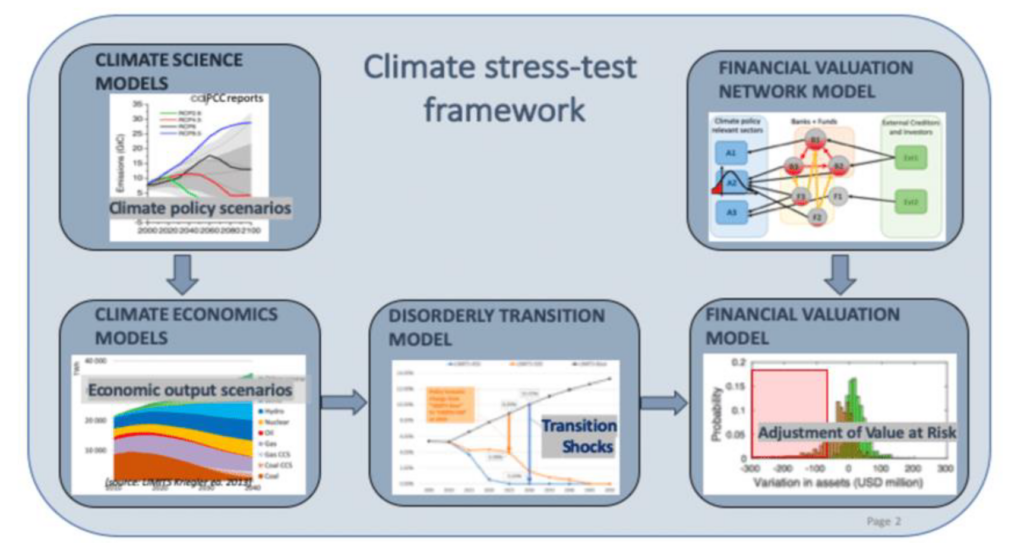

Effective risk management increasingly requires understanding how climate‑related factors can influence market valuations and balance‑sheet resilience. CRISK provides a transparent, market‑based… read more >>

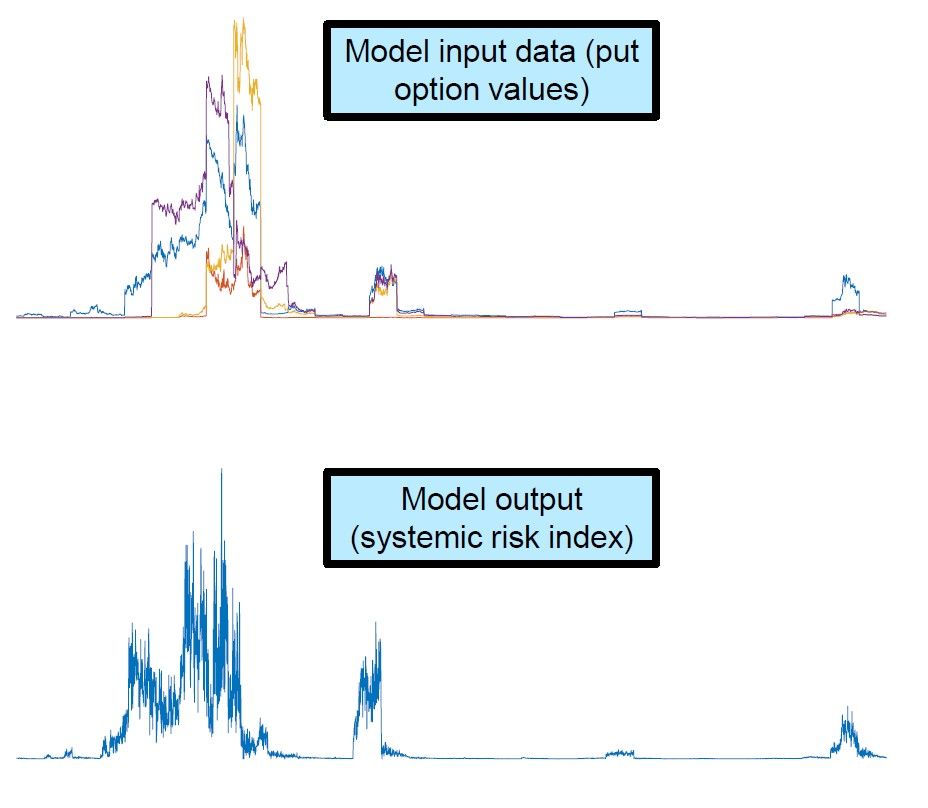

Systemic risk modeling is essential for central banks as financial systems grow more interconnected and vulnerable to sudden shocks. From market implied indicators to climate stress testing and… read more >>

“It [MATLAB] was used in Dynare in order to promote the accuracy and the ease of generating this model.”— Allan Wright, Manager, Central Bank of the Bahamas

Watch the Full… read more >>

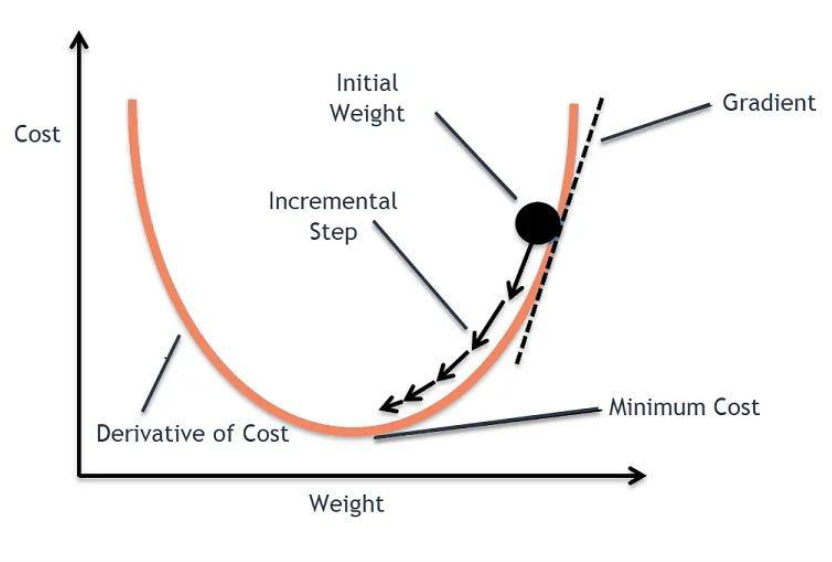

Dynamic Stochastic General Equilibrium (DSGE) models are essential tools for policy analysis and forecasting, but estimation runs often exceed 24 hours—particularly for large-scale models or Bayesian… read more >>

The 2025 MathWorks Finance Conference brought together quants, economists, financial modelers and researchers to explore how MATLAB is shaping the future of finance. Across two days, speakers shared… read more >>

If you work with macro, markets, or policy analysis, chances are you touch FRED®—the Federal Reserve Economic Data service. The Datafeed Toolbox gives you a first-class, native connector to FRED that… read more >>