A practical MATLAB walkthrough comparing tracking error and exact exposure approaches.

When you build a factor-based portfolio, the central design choice is how strictly to enforce your factor… 更多内容 >>

A practical MATLAB walkthrough comparing tracking error and exact exposure approaches.

When you build a factor-based portfolio, the central design choice is how strictly to enforce your factor… 更多内容 >>

Expert Contributor: Dr. Yuchen Dong

Yuchen is a Senior Application Engineer at MathWorks focusing on customers in the financial services industry. His focus areas are financial instruments,… 更多内容 >>

Expert Contributor: Dr. Eduard Benet Cerdà

Edu is a Senior Application Engineer at MathWorks advising customers in the development and deployment of financial applications. His focus… 更多内容 >>

R2026a covers a lot of ground for economists—Bayesian state-space estimation, macro-scale forecasting, climate and physical risk mapping, symbolic dynamics, and AI-assisted model review, among… 更多内容 >>

Every MATLAB release opens the door to new capabilities, better performance, and tighter integration with the platforms your team already uses. With two major releases a year and over 800… 更多内容 >>

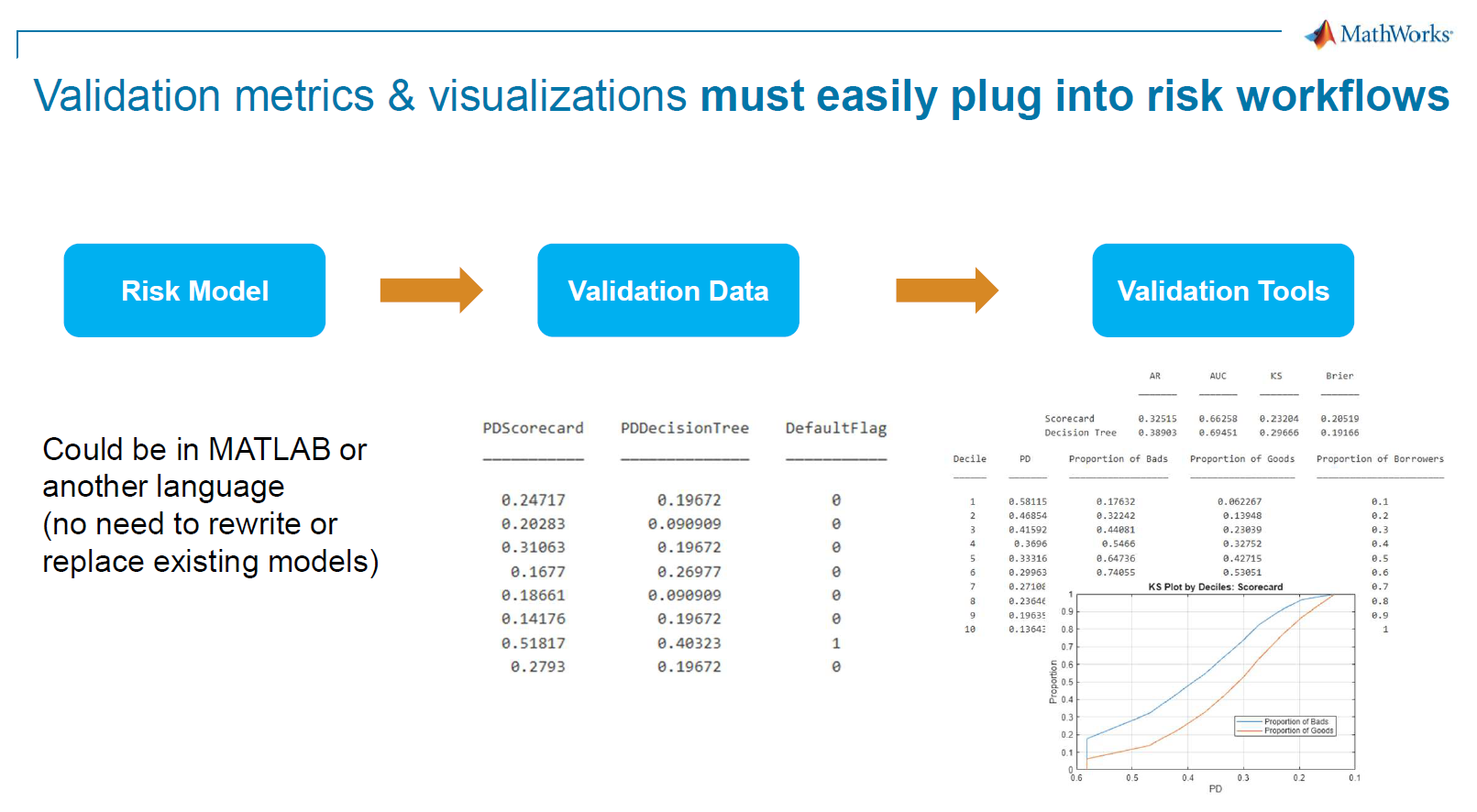

In this technical session, Valerio Sperandeo, Senior Application Engineer, demonstrated how MATLAB can support financial institutions in building robust, transparent, and scalable risk models aligned… 更多内容 >>

The 2025 MathWorks Finance Conference brought together quants, economists, financial modelers and researchers to explore how MATLAB is shaping the future of finance. Across two days, speakers shared… 更多内容 >>

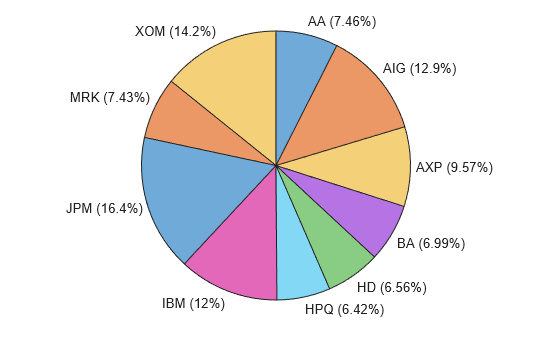

The following blog was written by Marshall Alphonso Principal Engineer and Sara Galante, Senior Finance Application Engineer at MathWorks

Watch the full webinar Custom Portfolio Optimization:… 更多内容 >>

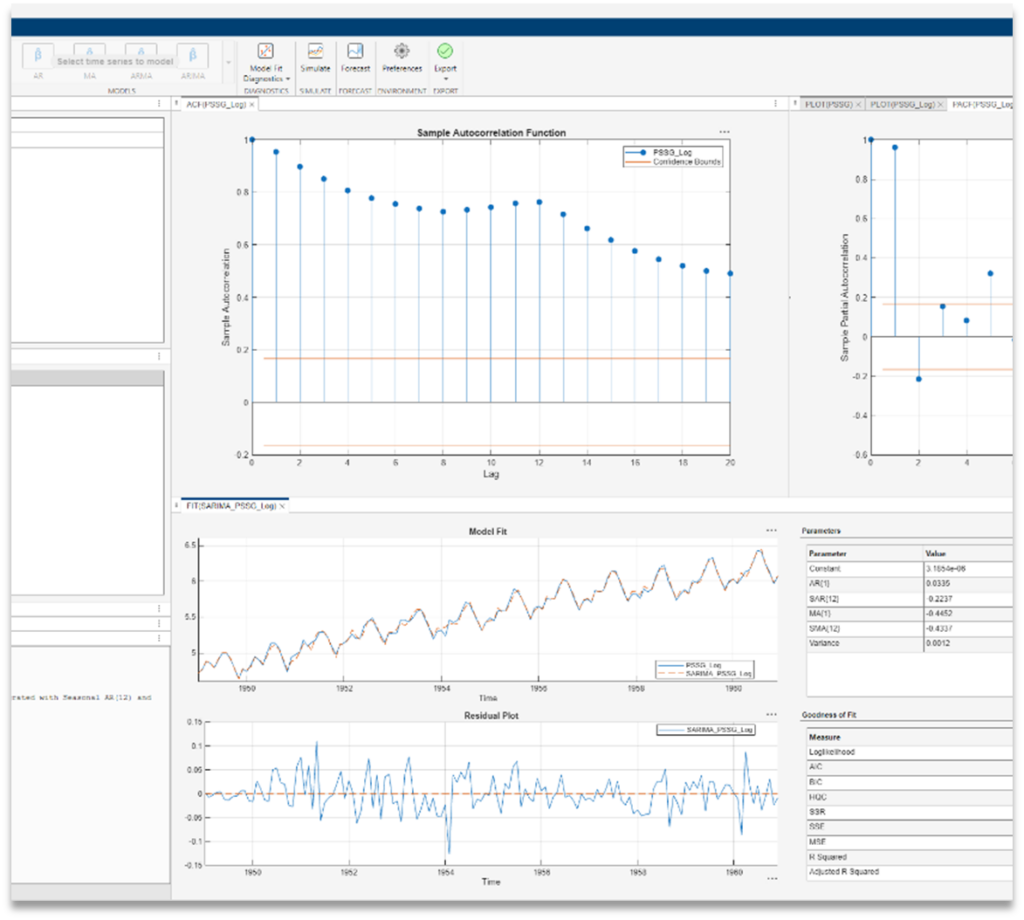

The following post is from Jue Liu from Columbia University and Yuchen Dong from MathWorks.

The example featured in the blog can be found on GitHub here.

View the Physics-Informed Neural Networks… 更多内容 >>

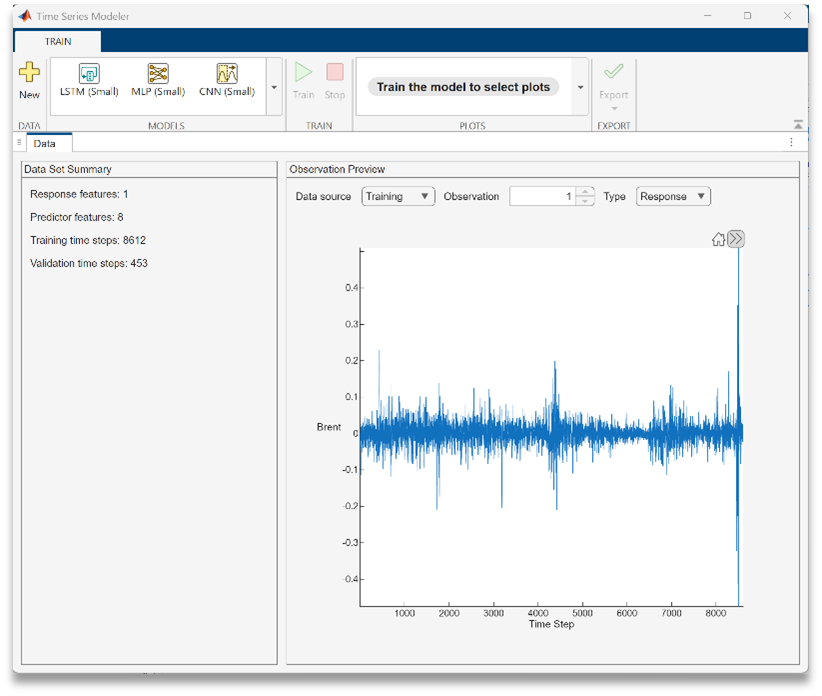

The following blog was written by Sara Galante, Senior Finance Application Engineer at Mathworks.

The GitHub documentation and MATLAB files are available here.

This blog demonstrates how MATLAB® and… 更多内容 >>